Permian Resources Announces Strong First Quarter 2025 Results, Revised 2025 Guidance and Strategic Bolt-On Acquisition of Core Northern Delaware Basin Assets

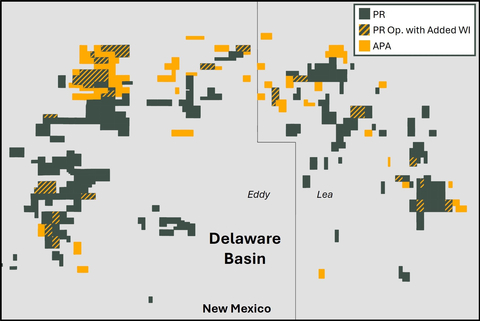

Permian Resources Acquired Acreage Map

Recent Financial and Operational Highlights

- Reported crude oil and total average production of 175.0 MBbls/d and 373.2 MBoe/d

-

Announced cash capital expenditures of

$501 million $898 million $460 million -

Closed previously announced non-core divestiture of the Barilla Draw gathering systems for

$180 million -

Maintained strong balance sheet with leverage1 of ~0.8x, cash of

$702 million $3.2 billion -

Declared base dividend of

$0.15 5.0% yield -

Recently repurchased 4.1 million shares at a weighted average price of

$10.52 -

Reduced the mid-point of full year capital budget by

$50 million $1.95 billion

Bolt-On Transaction Highlights

-

Acquired 13,320 net acres and 8,700 net royalty acres directly offset Permian Resources鈥� core

New Mexico operating areas for$608 million -

~12 MBoe/d (~

45% oil) of low decline production expected during second half of 2025 -

High NRI (average

83% 8/8ths) enhances returns and bolsters PR鈥檚 existing royalty position

-

~12 MBoe/d (~

-

Adds >100 new gross operated, two-mile locations with advantaged NRIs, which immediately compete for capital

-

Inventory scheduled for development in the near-term achieves an average breakeven of

~ per barrel WTI$30

-

Inventory scheduled for development in the near-term achieves an average breakeven of

-

Significant industrial logic with clear path to outsized value creation

-

Majority of inventory located within PR's existing Parkway asset in

Eddy County , one of the Company's most capital efficient assets - High-quality non-operated position provides PR the opportunity to add incremental value via its ground game

-

Majority of inventory located within PR's existing Parkway asset in

-

Purchased at an attractive valuation, reflecting current market conditions

-

$12,500 $6,000 $2 million - Accretive to all key per share metrics

-

-

Maintain strong balance sheet pro forma for transaction with <1x net debt-to-EBITDAX and >

$3 billion $60

Management Commentary

鈥淧ermian Resources delivered another outstanding quarter, highlighted by strong operational performance and lower costs. Through our team鈥檚 relentless pursuit of enhancing our low cost leadership, during the quarter we reduced controllable cash costs per Boe by

鈥淎s a result of the current environment, we are lowering the mid-point of our capital expenditure budget by

PR鈥檚 Fortress Balance Sheet Allows It To Be Opportunistic During Downturns

Since the Company鈥檚 inception, Permian Resources has been focused on improving its already strong balance sheet in order to position itself to create outsized value in the event of a downturn. Since year-end 2023, Permian Resources has increased its liquidity by over

Importantly, Permian Resources鈥� low-cost leadership and high-quality asset base have resulted in improved business fundamentals, capable of delivering strong free cash flow generation even at lower oil prices. Combined, these attributes ensure that Permian Resources is well-positioned to act in order to maximize shareholder returns in any commodity price environment.

Permian Resources鈥� downturn strategy is focused on three main pillars: maintaining a rock-solid balance sheet, leveraging its cost leadership and investing opportunistically. Given its current position of strength, the Company was able to immediately begin to execute on its downturn playbook during the second quarter, deploying capital in a countercyclical nature to take advantage of lower commodity prices. In April, the Company began to execute on its share repurchase program during heightened market volatility, buying back 4.1 million shares at a weighted average price of

Notably, the Company's balance sheet remains strong pro forma for the transaction, making it well positioned to continue executing upon this playbook, with expected net debt-to-EBITDAX of less than 1x and over

Financial and Operational Results

Permian Resources continued the efficient development of its core

Total cash capital expenditures (鈥渃apex鈥�) for the first quarter were

AG真人官方ized prices for the quarter were

For the first quarter, Permian Resources generated net cash provided by operating activities of

As previously discussed, Permian Resources continues to maintain a strong financial position and low leverage profile. During the quarter, the Company further strengthened its balance sheet by increasing cash on hand by

Acquisition Overview

Permian Resources announced that it has entered into a definitive agreement with APA Corporation (Nasdaq: APA) to purchase approximately 13,320 net acres, 8,700 net royalty acres and 12,000 Boe/d directly offset Permian Resources鈥� core

The bolt-on acquisition meets and exceeds Permian Resources鈥� acquisition criteria for growing its high-return and low breakeven inventory. Permian Resources has identified over 100 gross operated, two-mile locations with high NRIs which immediately compete for capital. The acquired inventory scheduled for development over the near-term achieves an average breakeven of

Permian Resources has identified significant upside potential associated with the acquired assets. In addition to new operated inventory, the acquisition increases working interest in over 100 existing Permian Resources operated locations, given the sizable acreage overlap. Additionally, the acquired properties include high-quality non-operated acreage adjacent to and surrounding Permian Resources鈥� current position. Utilizing its highly effective ground game, the Company plans to leverage this acreage to trade for incremental interests in existing operated units or establish new operating units.

鈥淭his acquisition is a natural fit for us and has material upside that Permian Resources is uniquely positioned to realize. We continue to grow our high return inventory, our net royalty acre portfolio and our acreage footprint in a cost-efficient manner that reflects the current environment. Our overarching goal is to drive long-term value for our investors, and we believe the addition of high-quality assets adjacent to our core position, acquired during a lower commodity price environment will further enhance short and long-term returns for investors,鈥� said James Walter, Co-CEO.

2025 Operational Plan and Target Update

Permian Resources is maintaining its full year 2025 standalone oil and total production guidance ranges, while reducing its cash capex range by

The recent acquisition noted above is expected to add approximately 12,000 Boe/d (~

(For a detailed table summarizing Permian Resources鈥� revised 2025 operational and financial guidance, please see the Appendix of this press release.)

Shareholder Returns

Permian Resources announced today that its Board of Directors declared the Company鈥檚 second quarter 2025 base dividend of

Subsequent to quarter-end, Permian Resources took advantage of heightened market volatility to opportunistically repurchase its shares in the open market. During April, the Company repurchased 4.1 million shares for

Quarterly Report on Form 10-Q

Permian Resources鈥� financial statements and related footnotes will be available in its Quarterly Report on Form 10-Q for the quarter ended March 31, 2025, which is expected to be filed with the Securities and Exchange Commission (鈥淪EC鈥�) on May 8, 2025.

Conference Call and Webcast

Permian Resources will host an investor conference call on Thursday, May 8, 2025 at 9:00 a.m. Central (10:00 a.m. Eastern) to discuss first quarter 2025 operating and financial results. Interested parties may join the call by visiting Permian Resources鈥� website at and clicking on the webcast link or by dialing (800) 549-8228 (Conference ID: 27785) at least 15 minutes prior to the start of the call. A replay of the call will be available on the Company鈥檚 website or by phone at (888) 660-6264 (Passcode: 27785) for a 14-day period following the call.

About Permian Resources

Headquartered in

Cautionary Note Regarding Forward-Looking Statements

The information in this press release includes 鈥渇orward-looking statements鈥� within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical fact included in this press release, regarding our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. When used in this press release, the words 鈥渃ould,鈥� 鈥渕ay,鈥� 鈥渂elieve,鈥� 鈥渁nticipate,鈥� 鈥渋ntend,鈥� 鈥渆stimate,鈥� 鈥渆xpect,鈥� 鈥減roject,鈥� 鈥済oal,鈥� 鈥減lan,鈥� 鈥渢arget鈥� and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These forward-looking statements are based on management鈥檚 current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events.

Forward-looking statements may include statements about:

-

volatility of oil, natural gas and NGL prices or a prolonged period of low oil, natural gas or NGL prices and the effects of actions by, or disputes among or between, members of the Organization of Petroleum Exporting Countries (鈥淥PEC鈥�), such as

Saudi Arabia , and other oil and natural gas producing countries, such asRussia , with respect to production levels or other matters related to the price of oil, natural gas and NGLs; -

political and economic conditions and events in or affecting other producing regions or countries, including the

Middle East ,Russia ,Eastern Europe ,Africa andSouth America ; - our business strategy and future drilling plans;

- our reserves and our ability to replace the reserves we produce through drilling and property acquisitions;

- our drilling prospects, inventories, projects and programs;

- our financial strategy, return of capital program, leverage, liquidity and capital required for our development program;

- our realized oil, natural gas and NGL prices;

- the timing and amount of our future production of oil, natural gas and NGLs;

- our ability to identify, complete and effectively integrate acquisitions of properties, or businesses;

- our hedging strategy and results;

- our competition;

- our ability to obtain permits and governmental approvals;

- our compliance with government regulations, including those related to climate change as well as environmental, health and safety regulations and liabilities thereunder;

- our pending legal matters;

- the marketing and transportation of our oil, natural gas and NGLs;

- our leasehold or business acquisitions;

- cost of developing or operating our properties;

- our anticipated rate of return;

- general economic conditions;

- weather conditions in the areas where we operate;

- credit markets;

- our ability to make dividends, distributions and share repurchases;

- uncertainty regarding our future operating results;

- our plans, objectives, expectations and intentions contained in this press release that are not historical; and

- the other factors described in our most recent Annual Report on Form 10-K, and any updates to those factors set forth in our subsequent Quarterly Reports on Form 10-Q or Current Reports on Form 8-K.

We caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond our control, incident to the exploration for and development, production, gathering and sale of oil, natural gas and NGLs. Factors which could cause our actual results to differ materially from the results contemplated by forward-looking statements include, but are not limited to:

- commodity price volatility (including regional basis differentials);

- uncertainty inherent in estimating oil, natural gas and NGL reserves, including the impact of commodity price declines on the economic producibility of such reserves, and in projecting future rates of production;

- geographic concentration of our operations;

- lack of availability of drilling and production equipment and services;

- lack of transportation and storage capacity as a result of oversupply, government regulations or other factors;

- risks related to acquisitions we may make from time to time, including the risk that we may fail to integrate such acquisitions on the terms and timing contemplated, or at all, and/or to realize our strategy and plans to achieve the expected benefits of such acquisitions;

- competition in the oil and natural gas industry for assets, materials, qualified personnel and capital;

- drilling and other operating risks;

- environmental and climate related risks, including seasonal weather conditions;

-

regulatory changes, including those that may result from the

U.S. Supreme Court鈥檚 decision overturning the Chevron deference doctrine and that may impact environmental, energy, and natural resources regulation; - the possibility that the industry in which we operate may be subject to new or volatile local, state, and federal laws, regulations or policies that may affect our business (including additional taxes and changes in regulations and policies related to environmental, health, and safety, climate change, trade policy and tariffs) as a result of existing or developing political, environmental and social movements;

- restrictions on the use of water, including limits on the use of produced water and potential restrictions on the availability of water disposal facilities;

- availability of cash flow and access to capital;

- inflation;

- changes in our credit ratings or adverse changes in interest rates;

- changes in the financial strength of counterparties to our credit agreement and hedging contracts;

- the timing of development expenditures;

-

political and economic conditions and events in foreign oil and natural gas producing countries, including embargoes, continued hostilities in the

Middle East and other sustained military campaigns, including the conflict inIsrael and its surrounding areas, the war inUkraine and associated economic sanctions onRussia , conditions inSouth America ,Central America ,China andRussia , and acts of terrorism or sabotage and the effects therefrom; - changes in local, regional, national, and international economic conditions;

- security threats, including evolving cybersecurity risks such as those involving unauthorized access, denial-of-service attacks, third-party service provider failures, malicious software, data privacy breaches by employees, insiders or other with authorized access, cyber or phishing-attacks, ransomware, social engineering, physical breaches or other actions; and

- other risks described in our filings with the SEC.

Reserve engineering is a process of estimating underground accumulations of oil and natural gas that cannot be measured in an exact way. The accuracy of any reserve estimate depends on the quality of available data, the interpretation of such data, and price and cost assumptions made by reserve engineers. In addition, the results of drilling, testing and production activities may justify revisions of estimates that were made previously. If significant, such revisions would change the schedule of any further production and development drilling. Accordingly, reserve estimates may differ significantly from the quantities of oil and natural gas that are ultimately recovered.

Should one or more of the risks or uncertainties described in this press release occur, or should any underlying assumptions prove incorrect, our actual results and plans could differ materially from those expressed in any forward-looking statements. All forward-looking statements, expressed or implied, included in this press release are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue.

Except as otherwise required by applicable law, we disclaim any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this press release.

1) Adjusted Operating Cash Flow, Adjusted Free Cash Flow, Adjusted Diluted Weighted Average Shares Outstanding and Net Debt-to-LQA EBITDAX (also referred to as 鈥渓everage鈥� in this press release) are non-GAAP financial measures. See 鈥淣on-GAAP Financial Measures鈥� included within the Appendix of this press release for related disclosures and reconciliations to the most directly comparable financial measures calculated and presented in accordance with GAAP. The Company does not provide guidance on the items used to reconcile between forecasted Net Debt-to-EBITDAX to forecasted long-term debt, net or forecasted net income due to the uncertainty regarding timing and estimates of certain items. Therefore, we cannot reconcile forecasted Net Debt-to-EBITDAX to long-term debt, net, or net income without unreasonable effort.

Details of our revised 2025 operational and financial guidance are presented below:

听 |

2025 FY Guidance

|

||||

Net average daily production (Boe/d) |

360,000 |

鈥� |

380,000 |

||

Net average daily oil production (Bbls/d) |

170,000 |

鈥� |

175,000 |

||

听 |

听 |

听 |

听 |

||

Production costs |

听 |

听 |

听 |

||

Total controllable cash costs |

|

鈥� |

|

||

Lease operating expenses ($/Boe) |

|

||||

Gathering, processing and transportation expenses ($/Boe) |

|

||||

Cash general and administrative ($/Boe)(1) |

|

||||

Severance and ad valorem taxes (% of revenue) |

|

鈥� |

|

||

听 |

听 |

听 |

听 |

||

Total cash capital expenditure program ($MM) |

|

鈥� |

|

||

听 |

听 |

听 |

听 |

||

Operated drilling program |

听 |

听 |

听 |

||

TILs (gross) |

~275 |

||||

Average working interest |

~ |

||||

Average lateral length (feet) |

~10,000 |

||||

(1) Excludes stock-based compensation. |

|||||

Permian Resources Corporation Operating Highlights |

||||||

| 听 | ||||||

听 |

Three Months Ended March 31, |

|||||

听 |

听 |

2025 |

听 |

听 |

2024 |

听 |

Net revenues (in thousands): |

听 |

听 |

听 |

|||

Oil sales |

$ |

1,109,771 |

听 |

$ |

1,051,642 |

听 |

Natural gas sales |

听 |

81,658 |

听 |

听 |

38,767 |

听 |

NGL sales |

听 |

185,022 |

听 |

听 |

152,590 |

听 |

Oil and gas sales |

$ |

1,376,451 |

听 |

$ |

1,242,999 |

听 |

听 |

听 |

听 |

听 |

|||

Net production: |

听 |

听 |

听 |

|||

Oil (MBbls) |

听 |

15,747 |

听 |

听 |

13,813 |

听 |

Natural gas (MMcf) |

听 |

60,605 |

听 |

听 |

51,802 |

听 |

NGL (MBbls) |

听 |

7,741 |

听 |

听 |

6,629 |

听 |

Total (MBoe)(1) |

听 |

33,589 |

听 |

听 |

29,076 |

听 |

听 |

听 |

听 |

听 |

|||

Average daily net production: |

听 |

听 |

听 |

|||

Oil (Bbls/d) |

听 |

174,967 |

听 |

听 |

151,794 |

听 |

Natural gas (Mcf/d) |

听 |

673,388 |

听 |

听 |

569,249 |

听 |

NGL (Bbls/d) |

听 |

86,010 |

听 |

听 |

72,846 |

听 |

Total (Boe/d)(1) |

听 |

373,209 |

听 |

听 |

319,514 |

听 |

听 |

听 |

听 |

听 |

|||

Average sales prices: |

听 |

听 |

听 |

|||

Oil (per Bbl) |

$ |

70.48 |

听 |

$ |

76.13 |

听 |

Effect of derivative settlements on average price (per Bbl) |

听 |

0.97 |

听 |

听 |

(0.12 |

) |

Oil including the effects of hedging (per Bbl) |

$ |

71.45 |

听 |

$ |

76.01 |

听 |

听 |

听 |

听 |

听 |

|||

Natural gas (per Mcf) |

$ |

1.35 |

听 |

$ |

0.75 |

听 |

Effect of derivative settlements on average price (per Mcf) |

听 |

0.10 |

听 |

听 |

0.17 |

听 |

Natural gas including the effects of hedging (per Mcf) |

$ |

1.45 |

听 |

$ |

0.92 |

听 |

听 |

听 |

听 |

听 |

|||

NGL (per Bbl) |

$ |

23.90 |

听 |

$ |

23.02 |

听 |

| __________ | ||

(1) |

Calculated by converting natural gas to oil equivalent barrels at a ratio of six Mcf of natural gas to one Boe. |

|

| 听 | |||||||

Permian Resources Corporation Operating Expenses |

|||||||

听 |

Three Months Ended March 31, |

||||||

听 |

听 |

2025 |

听 |

听 |

听 |

2024 |

听 |

Operating costs (in thousands): |

听 |

听 |

听 |

||||

Lease operating expenses |

$ |

179,627 |

听 |

听 |

$ |

168,671 |

听 |

Severance and ad valorem taxes |

听 |

107,993 |

听 |

听 |

听 |

96,166 |

听 |

Gathering, processing and transportation expenses |

听 |

46,650 |

听 |

听 |

听 |

39,055 |

听 |

Operating cost metrics: |

听 |

听 |

听 |

||||

Lease operating expenses (per Boe) |

$ |

5.35 |

听 |

听 |

$ |

5.80 |

听 |

Severance and ad valorem taxes (% of revenue) |

听 |

7.8 |

% |

听 |

听 |

7.7 |

% |

Gathering, processing and transportation expenses (per Boe) |

$ |

1.39 |

听 |

听 |

$ |

1.34 |

听 |

| 听 | |||||||

Permian Resources Corporation Consolidated Statements of Operations (unaudited) (in thousands, except per share data) |

|||||||

听 |

Three Months Ended March 31, |

||||||

听 |

听 |

2025 |

听 |

听 |

听 |

2024 |

听 |

Operating revenues |

听 |

听 |

听 |

||||

Oil and gas sales |

$ |

1,376,451 |

听 |

听 |

$ |

1,242,999 |

听 |

Operating expenses |

听 |

听 |

听 |

||||

Lease operating expenses |

听 |

179,627 |

听 |

听 |

听 |

168,671 |

听 |

Severance and ad valorem taxes |

听 |

107,993 |

听 |

听 |

听 |

96,166 |

听 |

Gathering, processing and transportation expenses |

听 |

46,650 |

听 |

听 |

听 |

39,055 |

听 |

Depreciation, depletion and amortization |

听 |

474,203 |

听 |

听 |

听 |

410,179 |

听 |

General and administrative expenses |

听 |

43,056 |

听 |

听 |

听 |

37,373 |

听 |

Merger and integration expense |

听 |

鈥� |

听 |

听 |

听 |

11,123 |

听 |

Impairment and abandonment expense |

听 |

5,209 |

听 |

听 |

听 |

20 |

听 |

Exploration and other expenses |

听 |

15,250 |

听 |

听 |

听 |

11,488 |

听 |

Total operating expenses |

听 |

871,988 |

听 |

听 |

听 |

774,075 |

听 |

Net gain on sale of long-lived assets |

听 |

鈥� |

听 |

听 |

听 |

112 |

听 |

Income from operations |

听 |

504,463 |

听 |

听 |

听 |

469,036 |

听 |

听 |

听 |

听 |

听 |

||||

Other income (expense) |

听 |

听 |

听 |

||||

Interest expense |

听 |

(79,665 |

) |

听 |

听 |

(72,587 |

) |

Net gain (loss) on derivative instruments |

听 |

57,731 |

听 |

听 |

听 |

(121,129 |

) |

Other income (expense) |

听 |

8,368 |

听 |

听 |

听 |

3,232 |

听 |

Total other income (expense) |

听 |

(13,566 |

) |

听 |

听 |

(190,484 |

) |

听 |

听 |

听 |

听 |

||||

Income before income taxes |

听 |

490,897 |

听 |

听 |

听 |

278,552 |

听 |

Income tax expense |

听 |

(100,334 |

) |

听 |

听 |

(48,957 |

) |

Net income |

听 |

390,563 |

听 |

听 |

听 |

229,595 |

听 |

Less: Net income attributable to noncontrolling interest |

听 |

(61,265 |

) |

听 |

听 |

(83,020 |

) |

Net income attributable to Class A Common Stock |

$ |

329,298 |

听 |

听 |

$ |

146,575 |

听 |

听 |

听 |

听 |

听 |

||||

Income per share of Class A Common Stock: |

听 |

听 |

听 |

||||

Basic |

$ |

0.47 |

听 |

听 |

$ |

0.27 |

听 |

Diluted |

$ |

0.44 |

听 |

听 |

$ |

0.25 |

听 |

听 |

听 |

听 |

听 |

||||

Weighted average Class A Common Stock outstanding: |

听 |

听 |

听 |

||||

Basic |

听 |

704,035 |

听 |

听 |

听 |

552,472 |

听 |

Diluted |

听 |

748,197 |

听 |

听 |

听 |

595,352 |

听 |

| 听 | |||||||

Permian Resources Corporation Consolidated Balance Sheets (unaudited) (in thousands, except share and per share amounts) |

|||||||

听 |

March 31,

|

听 |

December 31,

|

||||

ASSETS |

听 |

听 |

听 |

||||

Current assets |

听 |

听 |

听 |

||||

Cash and cash equivalents |

$ |

702,236 |

听 |

听 |

$ |

479,343 |

听 |

Accounts receivable, net |

听 |

528,593 |

听 |

听 |

听 |

530,452 |

听 |

Derivative instruments |

听 |

102,229 |

听 |

听 |

听 |

85,509 |

听 |

Prepaid and other current assets |

听 |

23,775 |

听 |

听 |

听 |

26,290 |

听 |

Total current assets |

听 |

1,356,833 |

听 |

听 |

听 |

1,121,594 |

听 |

Property and Equipment |

听 |

听 |

听 |

||||

Oil and natural gas properties, successful efforts method |

听 |

听 |

听 |

||||

Unproved properties |

听 |

1,911,988 |

听 |

听 |

听 |

1,990,441 |

听 |

Proved properties |

听 |

19,025,246 |

听 |

听 |

听 |

18,595,780 |

听 |

Accumulated depreciation, depletion and amortization |

听 |

(5,628,670 |

) |

听 |

听 |

(5,163,124 |

) |

Total oil and natural gas properties, net |

听 |

15,308,564 |

听 |

听 |

听 |

15,423,097 |

听 |

Other property and equipment, net |

听 |

50,432 |

听 |

听 |

听 |

50,381 |

听 |

Total property and equipment, net |

听 |

15,358,996 |

听 |

听 |

听 |

15,473,478 |

听 |

Noncurrent assets |

听 |

听 |

听 |

||||

Operating lease right-of-use assets |

听 |

150,923 |

听 |

听 |

听 |

119,703 |

听 |

Other noncurrent assets |

听 |

209,691 |

听 |

听 |

听 |

183,125 |

听 |

TOTAL ASSETS |

$ |

17,076,443 |

听 |

听 |

$ |

16,897,900 |

听 |

LIABILITIES AND EQUITY |

听 |

听 |

听 |

||||

Current liabilities |

听 |

听 |

听 |

||||

Accounts payable and accrued expenses |

$ |

1,151,049 |

听 |

听 |

$ |

1,198,418 |

听 |

Current portion of long-term debt |

听 |

288,603 |

听 |

听 |

听 |

鈥� |

听 |

Operating lease liabilities |

听 |

70,043 |

听 |

听 |

听 |

57,216 |

听 |

Other current liabilities |

听 |

75,577 |

听 |

听 |

听 |

71,703 |

听 |

Total current liabilities |

听 |

1,585,272 |

听 |

听 |

听 |

1,327,337 |

听 |

Noncurrent liabilities |

听 |

听 |

听 |

||||

Long-term debt, net |

听 |

3,710,381 |

听 |

听 |

听 |

4,184,233 |

听 |

Asset retirement obligations |

听 |

150,143 |

听 |

听 |

听 |

148,443 |

听 |

Deferred income taxes |

听 |

699,746 |

听 |

听 |

听 |

602,379 |

听 |

Operating lease liabilities |

听 |

82,636 |

听 |

听 |

听 |

64,288 |

听 |

Other noncurrent liabilities |

听 |

44,465 |

听 |

听 |

听 |

52,701 |

听 |

Total liabilities |

听 |

6,272,643 |

听 |

听 |

听 |

6,379,381 |

听 |

Shareholders鈥� equity |

听 |

听 |

听 |

||||

Common stock, |

听 |

听 |

听 |

||||

Class A: 710,078,422 shares issued and 704,872,781 shares outstanding at March 31, 2025 and 707,388,380 shares issued and 703,774,082 shares outstanding at December 31, 2024 |

听 |

71 |

听 |

听 |

听 |

71 |

听 |

Class C: 99,050,810 shares issued and outstanding at March 31, 2025 and 99,599,640 shares issued and outstanding at December 31, 2024 |

听 |

10 |

听 |

听 |

听 |

10 |

听 |

Additional paid-in capital |

听 |

8,080,421 |

听 |

听 |

听 |

8,056,552 |

听 |

Retained earnings (accumulated deficit) |

听 |

1,303,674 |

听 |

听 |

听 |

1,081,895 |

听 |

Total shareholders' equity |

听 |

9,384,176 |

听 |

听 |

听 |

9,138,528 |

听 |

Noncontrolling interest |

听 |

1,419,624 |

听 |

听 |

听 |

1,379,991 |

听 |

Total equity |

听 |

10,803,800 |

听 |

听 |

听 |

10,518,519 |

听 |

TOTAL LIABILITIES AND EQUITY |

$ |

17,076,443 |

听 |

听 |

$ |

16,897,900 |

|

| 听 | |||||||

Permian Resources Corporation Consolidated Statements of Cash Flows (unaudited) (in thousands) |

|||||||

| 听 | |||||||

听 |

Three Months Ended March 31, |

||||||

听 |

听 |

2025 |

听 |

听 |

听 |

2024 |

听 |

Cash flows from operating activities: |

听 |

听 |

听 |

||||

Net income |

$ |

390,563 |

听 |

听 |

$ |

229,595 |

听 |

Adjustments to reconcile net income to net cash provided by operating activities: |

听 |

听 |

听 |

||||

Depreciation, depletion and amortization |

听 |

474,203 |

听 |

听 |

听 |

410,179 |

听 |

Stock-based compensation expense |

听 |

16,929 |

听 |

听 |

听 |

9,631 |

听 |

Impairment and abandonment expense |

听 |

5,209 |

听 |

听 |

听 |

20 |

听 |

Deferred tax expense |

听 |

97,594 |

听 |

听 |

听 |

46,979 |

听 |

Net (gain) loss on sale of long-lived assets |

听 |

鈥� |

听 |

听 |

听 |

(112 |

) |

Non-cash portion of derivative (gain) loss |

听 |

(36,423 |

) |

听 |

听 |

128,474 |

听 |

Amortization of debt issuance costs, discount and premium |

听 |

2,139 |

听 |

听 |

听 |

1,531 |

听 |

Loss on extinguishment of debt |

听 |

5,826 |

听 |

听 |

听 |

鈥� |

听 |

Changes in operating assets and liabilities: |

听 |

听 |

听 |

||||

(Increase) decrease in accounts receivable |

听 |

14,177 |

听 |

听 |

听 |

(85,138 |

) |

(Increase) decrease in prepaid and other assets |

听 |

(8,853 |

) |

听 |

听 |

5,350 |

听 |

Increase (decrease) in accounts payable and other liabilities |

听 |

(63,332 |

) |

听 |

听 |

(98,911 |

) |

Net cash provided by operating activities |

听 |

898,032 |

听 |

听 |

听 |

647,598 |

听 |

Cash flows from investing activities: |

听 |

听 |

听 |

||||

Acquisition of oil and natural gas properties, net |

听 |

(35,401 |

) |

听 |

听 |

(97,019 |

) |

Drilling and development capital expenditures |

听 |

(500,732 |

) |

听 |

听 |

(519,623 |

) |

Purchases of other property and equipment |

听 |

(1,672 |

) |

听 |

听 |

(2,772 |

) |

Proceeds from sales of oil and natural gas properties |

听 |

175,989 |

听 |

听 |

听 |

66 |

听 |

Net cash used in investing activities |

听 |

(361,816 |

) |

听 |

听 |

(619,348 |

) |

Cash flows from financing activities: |

听 |

听 |

听 |

||||

Proceeds from borrowings under revolving credit facility |

听 |

鈥� |

听 |

听 |

听 |

220,000 |

听 |

Repayment of borrowings under revolving credit facility |

听 |

鈥� |

听 |

听 |

听 |

(160,000 |

) |

Redemption of senior notes |

听 |

(175,000 |

) |

听 |

听 |

鈥� |

听 |

Debt issuance and redemption costs |

听 |

(17,334 |

) |

听 |

听 |

(1,880 |

) |

Proceeds from exercise of stock options |

听 |

21 |

听 |

听 |

听 |

58 |

听 |

Share repurchases |

听 |

鈥� |

听 |

听 |

听 |

(31,492 |

) |

Dividends paid |

听 |

(106,070 |

) |

听 |

听 |

(87,194 |

) |

Distributions paid to noncontrolling interest owners |

听 |

(14,940 |

) |

听 |

听 |

(28,327 |

) |

Net cash used in financing activities |

听 |

(313,323 |

) |

听 |

听 |

(88,835 |

) |

Net increase (decrease) in cash, cash equivalents and restricted cash |

听 |

222,893 |

听 |

听 |

听 |

(60,585 |

) |

Cash, cash equivalents and restricted cash, beginning of period |

听 |

479,343 |

听 |

听 |

听 |

73,864 |

听 |

Cash, cash equivalents and restricted cash, end of period |

$ |

702,236 |

听 |

听 |

$ |

13,279 |

听 |

Reconciliation of cash, cash equivalents and restricted cash presented on the Consolidated Statements of Cash Flows for the periods presented:

听 |

Three Months Ended March 31, |

||||

听 |

听 |

2025 |

听 |

听 |

2024 |

Cash and cash equivalents |

$ |

702,236 |

听 |

$ |

12,692 |

Restricted cash |

听 |

鈥� |

听 |

听 |

587 |

Total cash, cash equivalents and restricted cash |

$ |

702,236 |

听 |

$ |

13,279 |

Non-GAAP Financial Measures

In addition to disclosing financial results calculated in accordance with

Adjusted EBITDAX

Adjusted EBITDAX is a supplemental non-GAAP financial measure that is used by management and external users of our consolidated financial statements, such as industry analysts, investors, lenders and rating agencies. We define Adjusted EBITDAX as net income attributable to Class A Common Stock before net income attributable to noncontrolling interest, interest expense, income taxes, depreciation, depletion and amortization, impairment and abandonment expense, non-cash gains or losses on derivatives, stock-based compensation, exploration and other expenses, merger and integration expense, gain/loss from the sale of long-lived assets and other non-recurring items. Adjusted EBITDAX is not a measure of net income as determined by GAAP.

Our management believes Adjusted EBITDAX is useful as it allows them to more effectively evaluate our operating performance and compare the results of our operations from period to period and against our peers, without regard to our financing methods or capital structure. We exclude the items listed above from net income in arriving at Adjusted EBITDAX because these amounts can vary substantially from company to company within our industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. Adjusted EBITDAX should not be considered as an alternative to, or more meaningful than, net income as determined in accordance with GAAP or as an indicator of our operating performance or liquidity. Certain items excluded from Adjusted EBITDAX are significant components in understanding and assessing a company鈥檚 financial performance, such as a company鈥檚 cost of capital and tax structure, as well as the historic costs of depreciable assets, none of which are components of Adjusted EBITDAX. Our presentation of Adjusted EBITDAX should not be construed as an inference that our results will be unaffected by unusual or nonrecurring items. Our computations of Adjusted EBITDAX may not be comparable to other similarly titled measures of other companies.

The following table presents a reconciliation of Adjusted EBITDAX to net income, which is the most directly comparable financial measure calculated and presented in accordance with GAAP:

听 |

Three Months Ended |

|||||||||||||||||

(in thousands) |

3/31/2025 |

听 |

12/31/2024 |

听 |

9/30/2024 |

听 |

6/30/2024 |

听 |

3/31/2024 |

|||||||||

Adjusted EBITDAX reconciliation to net income: |

听 |

听 |

听 |

听 |

听 |

听 |

听 |

听 |

听 |

|||||||||

Net income attributable to Class A Common Stock |

$ |

329,298 |

听 |

听 |

$ |

216,650 |

听 |

$ |

386,376 |

听 |

听 |

$ |

235,100 |

听 |

听 |

$ |

146,575 |

听 |

Net income attributable to noncontrolling interest |

听 |

61,265 |

听 |

听 |

听 |

38,829 |

听 |

听 |

70,151 |

听 |

听 |

听 |

73,808 |

听 |

听 |

听 |

83,020 |

听 |

Interest expense |

听 |

79,665 |

听 |

听 |

听 |

76,783 |

听 |

听 |

79,934 |

听 |

听 |

听 |

75,452 |

听 |

听 |

听 |

72,587 |

听 |

Income tax expense |

听 |

100,334 |

听 |

听 |

听 |

62,645 |

听 |

听 |

106,468 |

听 |

听 |

听 |

82,272 |

听 |

听 |

听 |

48,957 |

听 |

Depreciation, depletion and amortization |

听 |

474,203 |

听 |

听 |

听 |

486,463 |

听 |

听 |

453,603 |

听 |

听 |

听 |

426,428 |

听 |

听 |

听 |

410,179 |

听 |

Impairment and abandonment expense |

听 |

5,209 |

听 |

听 |

听 |

2,128 |

听 |

听 |

1,380 |

听 |

听 |

听 |

6,384 |

听 |

听 |

听 |

20 |

听 |

Non-cash derivative (gain) loss |

听 |

(36,423 |

) |

听 |

听 |

73,579 |

听 |

听 |

(213,102 |

) |

听 |

听 |

(6,734 |

) |

听 |

听 |

128,474 |

听 |

Stock-based compensation expense(1) |

听 |

16,199 |

听 |

听 |

听 |

13,149 |

听 |

听 |

13,537 |

听 |

听 |

听 |

22,463 |

听 |

听 |

听 |

9,094 |

听 |

Exploration and other expenses |

听 |

15,250 |

听 |

听 |

听 |

6,363 |

听 |

听 |

6,962 |

听 |

听 |

听 |

5,978 |

听 |

听 |

听 |

11,488 |

听 |

Merger and integration expense |

听 |

鈥� |

听 |

听 |

听 |

鈥� |

听 |

听 |

鈥� |

听 |

听 |

听 |

6,941 |

听 |

听 |

听 |

11,123 |

听 |

(Gain) loss on sale of long-lived assets |

听 |

鈥� |

听 |

听 |

听 |

66 |

听 |

听 |

(329 |

) |

听 |

听 |

鈥� |

听 |

听 |

听 |

(112 |

) |

Adjusted EBITDAX |

$ |

1,045,000 |

听 |

听 |

$ |

976,655 |

听 |

$ |

904,980 |

听 |

听 |

$ |

928,092 |

听 |

听 |

$ |

921,405 |

|

| _____________ | ||

(1) |

Includes stock-based compensation expense for equity awards related to general and administrative employees only. Stock-based compensation amounts for geographical and geophysical personnel are included within the Exploration and other expenses line item. |

|

Net Debt-to-LQA EBITDAX

Net debt-to-LQA EBITDAX, also referred to as leverage, is a non-GAAP financial measure. We define net debt as total debt, net, plus unamortized debt discount, premium and debt issuance costs on our senior notes minus cash and cash equivalents.

We define net debt-to-LQA EBITDAX as net debt (defined above) divided by Adjusted EBITDAX (defined and reconciled in the section above) for the three months ended March 31, 2025, on an annualized basis. We refer to this metric to show trends that investors may find useful in understanding our ability to service our debt. This metric is widely used by professional research analysts, including credit analysts, in the valuation and comparison of companies in the oil and gas exploration and production industry. The following table presents a reconciliation of net debt to total debt, net and the calculation of net debt-to-LQA EBITDAX for the period presented:

(in thousands) |

March 31, 2025 |

||

Total debt, net |

$ |

3,998,984 |

听 |

Unamortized debt discount, premium and issuance costs on senior notes |

听 |

35,464 |

听 |

Total debt |

听 |

4,034,448 |

听 |

Less: cash and cash equivalents |

听 |

(702,236 |

) |

Net debt (Non-GAAP) |

听 |

3,332,212 |

听 |

LQA EBITDAX(1) |

听 |

4,180,000 |

听 |

Net debt-to-LQA EBITDAX |

听 |

0.8 |

|

(1) |

Represents adjusted EBITDAX (defined and reconciled in the section above) for the three months ended March 31, 2025, on an annualized basis. |

Adjusted Shares

Adjusted basic and diluted weighted average shares outstanding (鈥淎djusted Basic and Diluted Shares鈥�) are non-GAAP financial measures defined as basic and diluted weighted average shares outstanding adjusted to reflect the weighted average shares of our Class C Common Stock outstanding during the period.

Our Adjusted Basic and Diluted Shares provide a comparable per share measurement when presenting results such as adjusted free cash flow and adjusted net income that include the interests of both net income attributable to Class A Common Stock and the net income attributable to our noncontrolling interest. Adjusted Basic and Diluted Shares are used in calculating several metrics that we use as supplemental financial measurements in the evaluation of our business.

The following table presents a reconciliation of Adjusted Basic and Diluted Shares to basic and diluted weighted average shares outstanding, which are the most directly comparable financial measure calculated and presented in accordance with GAAP:

听 |

Three Months Ended March 31, |

||

(in thousands) |

2025 |

听 |

2024 |

Basic weighted average shares of Class A Common Stock outstanding |

704,035 |

听 |

552,472 |

Weighted average shares of Class C Common Stock |

99,594 |

听 |

218,811 |

Adjusted basic weighted average shares outstanding |

803,629 |

听 |

771,283 |

听 |

听 |

听 |

听 |

Basic weighted average shares of Class A Common Stock outstanding |

704,035 |

听 |

552,472 |

Add: Dilutive effects of Convertible Senior Notes |

29,753 |

听 |

28,355 |

Add: Dilutive effects of equity awards |

14,409 |

听 |

14,525 |

Diluted weighted average shares of Class A Common Stock outstanding |

748,197 |

听 |

595,352 |

Weighted average shares of Class C Common Stock |

99,594 |

听 |

218,811 |

Adjusted diluted weighted average shares outstanding |

847,791 |

听 |

814,163 |

Adjusted Operating Cash Flow and Adjusted Free Cash Flow

Adjusted operating cash flow and adjusted free cash flow are supplemental non-GAAP financial measures used by management and external users of our consolidated financial statements, such as industry analysts, investors, lenders and rating agencies. We define adjusted operating cash flow as net cash provided by operating activities adjusted to remove changes in working capital, merger and integration and other non-recurring charges, and estimated tax distributions to our non-controlling interest owners. Adjusted operating cash flows is reduced by total cash capital expenditures to arrive at adjusted free cash flows.

Our management believes adjusted operating cash flow and adjusted free cash flow are useful indicators of the Company鈥檚 ability to internally fund its future exploration and development activities, to service its existing level of indebtedness or incur additional debt, without regard to the timing of settlement of either operating assets and liabilities, its merger and integration and other non-recurring costs or estimated tax distributions to noncontrolling interest owners after funding its capital expenditures paid for the period. The Company believes that these measures, as so adjusted, present meaningful indicators of the Company鈥檚 actual sources and uses of capital associated with its operations conducted during the applicable period. Our computation of adjusted operating cash flow and adjusted free cash flow may not be comparable to other similarly titled measures of other companies. Adjusted operating cash flow and adjusted free cash flow should not be considered as alternatives to, or more meaningful than, net cash provided by operating activities as determined in accordance with GAAP or as indicators of our operating performance or liquidity.

Adjusted operating cash flow and adjusted free cash flow are not financial measures that are determined in accordance with GAAP. Accordingly, the following table presents a reconciliation of adjusted operating cash flow and adjusted free cash flow to net cash provided by operating activities, which is the most directly comparable financial measure calculated and presented in accordance with GAAP:

听 |

Three Months Ended March 31, |

||||||

(in thousands, except per share data) |

听 |

2025 |

听 |

听 |

听 |

2024 |

听 |

Net cash provided by operating activities |

$ |

898,032 |

听 |

听 |

$ |

647,598 |

听 |

Changes in working capital: |

听 |

听 |

听 |

||||

Accounts receivable |

听 |

(14,177 |

) |

听 |

听 |

85,138 |

听 |

Prepaid and other assets |

听 |

8,853 |

听 |

听 |

听 |

(5,350 |

) |

Accounts payable and other liabilities |

听 |

63,332 |

听 |

听 |

听 |

98,911 |

听 |

Merger and integration expense & other |

听 |

4,749 |

听 |

听 |

听 |

17,612 |

听 |

Estimated tax distribution to noncontrolling interest owners(1) |

听 |

(252 |

) |

听 |

听 |

(335 |

) |

Adjusted operating cash flow |

听 |

960,537 |

听 |

听 |

听 |

843,574 |

听 |

Less: total cash capital expenditures |

听 |

(500,732 |

) |

听 |

听 |

(519,623 |

) |

Adjusted free cash flow |

$ |

459,805 |

听 |

听 |

$ |

323,951 |

听 |

听 |

听 |

听 |

听 |

||||

Adjusted diluted weighted average shares outstanding |

听 |

847,791 |

听 |

听 |

听 |

814,163 |

|

| ___________ | ||

(1) |

Reflects estimated future distributions to noncontrolling interest owners based upon current federal and state income tax expense recognized during the period and expected to be paid by the partnership. Such estimates are based upon the noncontrolling interest ownership percentage as of the three months ended March 31, 2025. |

|

Adjusted Net Income

Adjusted net income is a supplemental non-GAAP financial measure that is used by management and external users of our consolidated financial statements, such as industry analysts, investors, lenders and rating agencies. We define adjusted net income as net income attributable to Class A Common Stock plus net income attributable to noncontrolling interest adjusted for non-cash gains or losses on derivatives, merger and integration expense, other nonrecurring charges, impairment and abandonment expense, gain/loss from the sale of long-lived assets and the related income tax adjustments for these items. Adjusted net income is not a measure of net income as determined by GAAP.

Our management believes adjusted net income is useful as it allows them to more effectively evaluate our operating performance and compare the results of our operations from period to period and against our peers by excluding certain non-cash items that can vary significantly. Adjusted net income should not be considered as an alternative to, or more meaningful than, net income as determined in accordance with GAAP or as an indicator of our operating performance or liquidity. Our presentation of adjusted net income should not be construed as an inference that our results will be unaffected by unusual or nonrecurring items. Our computations of adjusted net income may not be comparable to other similarly titled measures of other companies.

Adjusted net income is not a financial measure that is determined in accordance with GAAP. Accordingly, the following table presents a reconciliation of adjusted net income to net income, which is the most directly comparable financial measure calculated and presented in accordance with GAAP:

听 |

Three Months Ended March 31, |

||||||

(in thousands, except per share data) |

听 |

2025 |

听 |

听 |

听 |

2024 |

听 |

Net income attributable to Class A Common Stock |

$ |

329,298 |

听 |

听 |

$ |

146,575 |

听 |

Net income attributable to noncontrolling interest |

听 |

61,265 |

听 |

听 |

听 |

83,020 |

听 |

Non-cash derivative (gain) loss |

听 |

(36,423 |

) |

听 |

听 |

128,474 |

听 |

Merger and integration expense & other |

听 |

4,749 |

听 |

听 |

听 |

17,612 |

听 |

Impairment and abandonment expense |

听 |

5,209 |

听 |

听 |

听 |

20 |

听 |

(Gain) loss on sale of long-lived assets |

听 |

鈥� |

听 |

听 |

听 |

(112 |

) |

Adjusted net income excluding above items |

听 |

364,098 |

听 |

听 |

听 |

375,589 |

听 |

Income tax benefit (expense) attributable to the above items(1) |

听 |

(7,830 |

) |

听 |

听 |

(51,528 |

) |

Adjusted net income |

$ |

356,268 |

听 |

听 |

$ |

324,061 |

听 |

Interest on Convertible Senior Notes, net of tax |

听 |

1,283 |

听 |

听 |

听 |

1,322 |

听 |

Adjusted Net Income - Diluted |

听 |

357,551 |

听 |

听 |

听 |

325,383 |

听 |

听 |

听 |

听 |

听 |

||||

Adjusted diluted weighted average shares outstanding (Non-GAAP)(2) |

听 |

847,791 |

听 |

听 |

听 |

814,163 |

听 |

Adjusted net income per adjusted diluted share |

$ |

0.42 |

听 |

听 |

$ |

0.40 |

听 |

| ___________ | ||

| (1) |

Income tax benefit (expense) for adjustments made to adjusted net income is calculated using PR's federal and state-apportioned statutory tax rate that was approximately |

|

| (2) | Adjusted diluted weighted average shares outstanding is a Non-GAAP measure that has been computed and reconciled to the nearest GAAP metric in the preceding table above. |

|

The following table summarizes the approximate volumes and average contract prices of the hedge contracts the Company had in place as of April 30, 2025:

听 |

Period |

听 |

Volume (Bbls) |

听 |

Volume (Bbls/d) |

听 |

Wtd. Avg. Crude

|

|

Crude oil swaps |

April 2025 - June 2025 |

听 |

4,095,000 |

听 |

45,000 |

听 |

|

|

听 |

July 2025 - September 2025 |

听 |

4,140,000 |

听 |

45,000 |

听 |

72.64 |

|

听 |

October 2025 - December 2025 |

听 |

4,140,000 |

听 |

45,000 |

听 |

71.60 |

|

听 |

January 2026 - March 2026 |

听 |

1,575,000 |

听 |

17,500 |

听 |

71.49 |

|

听 |

April 2026 - June 2026 |

听 |

1,592,500 |

听 |

17,500 |

听 |

70.61 |

|

听 |

July 2026 - September 2026 |

听 |

1,610,000 |

听 |

17,500 |

听 |

69.77 |

|

听 |

October 2026 - December 2026 |

听 |

1,610,000 |

听 |

17,500 |

听 |

69.08 |

听 |

Period |

听 |

Volume (Bbls) |

听 |

Volume (Bbls/d) |

听 |

Wtd. Avg.

|

|

Crude oil basis differential swaps |

April 2025 - June 2025 |

听 |

4,095,000 |

听 |

45,000 |

听 |

|

|

听 |

July 2025 - September 2025 |

听 |

4,140,000 |

听 |

45,000 |

听 |

1.10 |

|

听 |

October 2025 - December 2025 |

听 |

4,140,000 |

听 |

45,000 |

听 |

1.10 |

|

听 |

January 2026 - March 2026 |

听 |

1,575,000 |

听 |

17,500 |

听 |

1.15 |

|

听 |

April 2026 - June 2026 |

听 |

1,592,500 |

听 |

17,500 |

听 |

1.15 |

|

听 |

July 2026 - September 2026 |

听 |

1,610,000 |

听 |

17,500 |

听 |

1.15 |

|

听 |

October 2026 - December 2026 |

听 |

1,610,000 |

听 |

17,500 |

听 |

1.15 |

听 |

Period |

听 |

Volume (Bbls) |

听 |

Volume (Bbls/d) |

听 |

Wtd. Avg.

|

|

Crude oil roll differential swaps |

April 2025 - June 2025 |

听 |

4,095,000 |

听 |

45,000 |

听 |

|

|

听 |

July 2025 - September 2025 |

听 |

4,140,000 |

听 |

45,000 |

听 |

0.44 |

|

听 |

October 2025 - December 2025 |

听 |

4,140,000 |

听 |

45,000 |

听 |

0.44 |

|

听 |

January 2026 - March 2026 |

听 |

1,575,000 |

听 |

17,500 |

听 |

0.28 |

|

听 |

April 2026 - June 2026 |

听 |

1,592,500 |

听 |

17,500 |

听 |

0.28 |

|

听 |

July 2026 - September 2026 |

听 |

1,610,000 |

听 |

17,500 |

听 |

0.28 |

|

听 |

October 2026 - December 2026 |

听 |

1,610,000 |

听 |

17,500 |

听 |

0.28 |

| ___________ | ||

(1) |

These crude oil swap transactions are settled based on the NYMEX WTI index price on each trading day within the specified monthly settlement period versus the contractual swap price for the volumes stipulated. |

|

(2) |

These crude oil basis swap transactions are settled based on the difference between the arithmetic average of ARGUS |

|

(3) |

These crude oil roll swap transactions are settled based on the difference between the arithmetic average of NYMEX WTI calendar month prices and the physical crude oil delivery month price. |

|

听 |

Period |

听 |

Volume (MMBtu) |

听 |

Volume (MMBtu/d) |

听 |

Wtd. Avg. Gas Price ($/MMBtu)(1) |

|

Natural gas swaps - Henry Hub |

April 2025 - June 2025 |

听 |

11,193,000 |

听 |

123,000 |

听 |

|

|

听 |

July 2025 - September 2025 |

听 |

11,316,000 |

听 |

123,000 |

听 |

3.43 |

|

听 |

October 2025 - December 2025 |

听 |

11,316,000 |

听 |

123,000 |

听 |

3.85 |

|

听 |

January 2026 - March 2026 |

听 |

8,190,000 |

听 |

91,000 |

听 |

4.08 |

|

听 |

April 2026 - June 2026 |

听 |

8,281,000 |

听 |

91,000 |

听 |

3.40 |

|

听 |

July 2026 - September 2026 |

听 |

8,372,000 |

听 |

91,000 |

听 |

3.65 |

|

听 |

October 2026 - December 2026 |

听 |

8,372,000 |

听 |

91,000 |

听 |

4.01 |

|

听 |

January 2027 - March 2027 |

听 |

12,600,000 |

听 |

140,000 |

听 |

4.24 |

|

听 |

April 2027 - June 2027 |

听 |

12,740,000 |

听 |

140,000 |

听 |

3.32 |

|

听 |

July 2027 - September 2027 |

听 |

12,880,000 |

听 |

140,000 |

听 |

3.58 |

|

听 |

October 2027 - December 2027 |

听 |

12,880,000 |

听 |

140,000 |

听 |

3.94 |

听 |

Period |

听 |

Volume (MMBtu) |

听 |

Volume (MMBtu/d) |

听 |

Wtd. Avg. Gas Price ($/MMBtu)(2) |

|

Natural gas swaps - Waha Hub |

April 2025 - June 2025 |

听 |

7,015,000 |

听 |

77,088 |

听 |

|

|

听 |

July 2025 - September 2025 |

听 |

10,580,000 |

听 |

115,000 |

听 |

1.70 |

|

听 |

October 2025 - December 2025 |

听 |

7,530,000 |

听 |

81,848 |

听 |

1.41 |

|

听 |

January 2026 - March 2026 |

听 |

5,850,000 |

听 |

65,000 |

听 |

2.78 |

|

听 |

April 2026 - June 2026 |

听 |

5,915,000 |

听 |

65,000 |

听 |

0.27 |

|

听 |

July 2026 - September 2026 |

听 |

5,980,000 |

听 |

65,000 |

听 |

1.68 |

|

听 |

October 2026 - December 2026 |

听 |

12,385,000 |

听 |

134,620 |

听 |

2.68 |

|

听 |

January 2027 - March 2027 |

听 |

7,650,000 |

听 |

85,000 |

听 |

3.57 |

听 |

Period |

听 |

Volume (MMBtu) |

听 |

Volume (MMBtu/d) |

听 |

Wtd. Avg. Differential ($/MMBtu)(3) |

|

Natural gas basis differential swaps |

April 2025 - June 2025 |

听 |

11,193,000 |

听 |

123,000 |

听 |

|

|

听 |

July 2025 - September 2025 |

听 |

11,316,000 |

听 |

123,000 |

听 |

(1.23) |

|

听 |

October 2025 - December 2025 |

听 |

11,316,000 |

听 |

123,000 |

听 |

(1.25) |

|

听 |

January 2026 - March 2026 |

听 |

8,190,000 |

听 |

91,000 |

听 |

(1.09) |

|

听 |

April 2026 - June 2026 |

听 |

8,281,000 |

听 |

91,000 |

听 |

(2.27) |

|

听 |

July 2026 - September 2026 |

听 |

8,372,000 |

听 |

91,000 |

听 |

(1.29) |

|

听 |

October 2026 - December 2026 |

听 |

8,372,000 |

听 |

91,000 |

听 |

(0.98) |

|

听 |

January 2027 - March 2027 |

听 |

12,600,000 |

听 |

140,000 |

听 |

(0.46) |

|

听 |

April 2027 - June 2027 |

听 |

12,740,000 |

听 |

140,000 |

听 |

(1.11) |

|

听 |

July 2027 - September 2027 |

听 |

12,880,000 |

听 |

140,000 |

听 |

(0.62) |

|

听 |

October 2027 - December 2027 |

听 |

12,880,000 |

听 |

140,000 |

听 |

(0.87) |

| ___________ | ||||

(1) |

These natural gas swap contracts are settled based on the NYMEX Henry Hub price on each trading day within the specified monthly settlement period versus the contractual swap price for the volumes stipulated. |

|||

(2) |

These natural gas swap contracts are settled based on the Waha Hub daily price on each trading day within the specified monthly settlement period versus the contractual swap price for the volumes stipulated. |

|||

(3) |

These natural gas basis swap contracts are settled based on the difference between the Inside FERC鈥檚 West Texas Waha Hub price and the NYMEX price of natural gas, during each applicable monthly settlement period. |

|||

听

View source version on businesswire.com:

Hays Mabry 鈥� Vice President, Investor Relations

(432) 315-0114

[email protected]

Source: Permian Resources Corporation