Trinity Bank Reports 2025 2nd Quarter Net Income up 10.2% to $ 2,374,000 - Return on Assets 1.79%

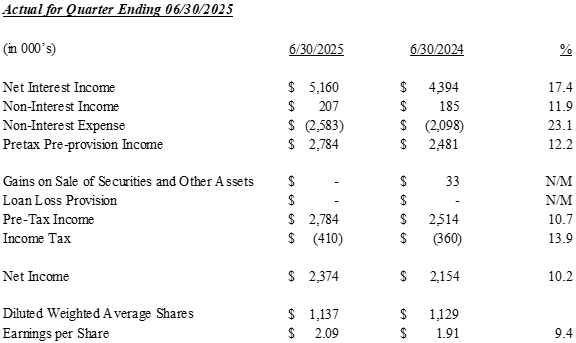

Trinity Bank (OTC PINK:TYBT) reported record Q2 2025 earnings with net income of $2.374 million, up 10.2% from Q2 2024. The bank achieved earnings per diluted share of $2.09, a 9.4% increase year-over-year.

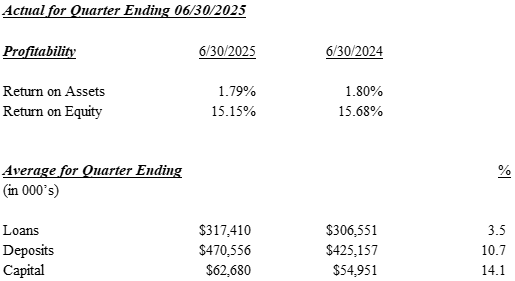

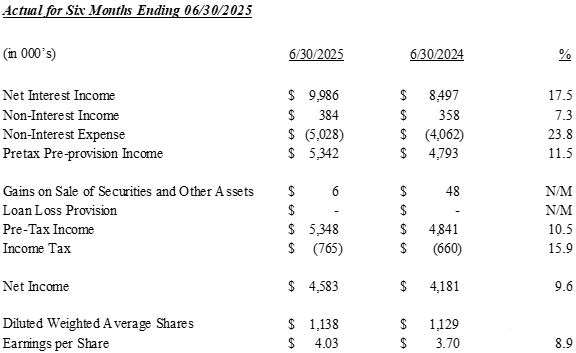

For the first half of 2025, net income reached $4.583 million, rising 9.6% compared to H1 2024, with diluted EPS of $4.03, up 8.7%. Key performance metrics include a strong return on assets of 1.79% and net interest margin of 4.21%. Total assets grew to $530.6 million, with total deposits increasing 10.7% to $470.6 million.

Trinity Bank (OTC PINK:TYBT) ha riportato risultati record per il secondo trimestre del 2025 con un utile netto di 2,374 milioni di dollari, in aumento del 10,2% rispetto al secondo trimestre del 2024. La banca ha raggiunto un utile per azione diluito di 2,09 dollari, con un incremento del 9,4% anno su anno.

Per la prima metà del 2025, l’utile netto ha raggiunto 4,583 milioni di dollari, crescendo del 9,6% rispetto al primo semestre 2024, con un utile per azione diluito di 4,03 dollari, in aumento dell��8,7%. I principali indicatori di performance includono un solido rendimento degli attivi dell��1,79% e un margine di interesse netto del 4,21%. Gli attivi totali sono cresciuti a 530,6 milioni di dollari, con depositi totali in aumento del 10,7% a 470,6 milioni di dollari.

Trinity Bank (OTC PINK:TYBT) reportó ganancias récord en el segundo trimestre de 2025 con un ingreso neto de 2,374 millones de dólares, un aumento del 10,2% respecto al segundo trimestre de 2024. El banco logró ganancias por acción diluida de 2,09 dólares, un incremento del 9,4% interanual.

Para el primer semestre de 2025, el ingreso neto alcanzó los 4,583 millones de dólares, aumentando un 9,6% en comparación con el primer semestre de 2024, con ganancias por acción diluida de 4,03 dólares, un aumento del 8,7%. Las métricas clave de desempeño incluyen un sólido retorno sobre activos del 1,79% y un margen neto de interés del 4,21%. Los activos totales crecieron a 530,6 millones de dólares, con depósitos totales aumentando un 10,7% hasta 470,6 millones de dólares.

트리니티 은��(OTC PINK:TYBT)은 2025�� 2분기�� 순이�� 237�� 4�� 달러�� 기록하며 2024�� 2분기 대�� 10.2% 증가�� 실적�� 발표했습니다. 희석 주당순이익은 2.09달러�� 전년 동기 대�� 9.4% 상승했습니다.

2025�� 상반�� 순이익은 458�� 3�� 달러�� 달하�� 2024�� 상반�� 대�� 9.6% 증가했고, 희석 주당순이익은 4.03달러�� 8.7% 상승했습니다. 주요 성과 지표로�� 견고�� 총자산수익률 1.79%왶� 순이자마�� 4.21%�� 포함됩니��. 총자산은 5�� 3,060�� 달러�� 증가했으��, �� 예금은 10.7% 증가�� 4�� 7,060�� 달러�� 기록했습니다.

Trinity Bank (OTC PINK:TYBT) a annoncé des résultats records pour le deuxième trimestre 2025 avec un revenu net de 2,374 millions de dollars, en hausse de 10,2 % par rapport au deuxième trimestre 2024. La banque a réalisé un bénéfice par action dilué de 2,09 dollars, soit une augmentation de 9,4 % d'une année sur l'autre.

Pour le premier semestre 2025, le revenu net a atteint 4,583 millions de dollars, en hausse de 9,6 % par rapport au premier semestre 2024, avec un bénéfice par action dilué de 4,03 dollars, en progression de 8,7 %. Les indicateurs clés de performance incluent un solide rendement des actifs de 1,79 % et une marge nette d’intérêt de 4,21 %. Le total des actifs a augmenté pour atteindre 530,6 millions de dollars, les dépôts totaux ayant progressé de 10,7 % pour atteindre 470,6 millions de dollars.

Trinity Bank (OTC PINK:TYBT) meldete Rekordgewinne für das zweite Quartal 2025 mit einem Nettoeinkommen von 2,374 Millionen US-Dollar, was einem Anstieg von 10,2 % gegenüber dem zweiten Quartal 2024 entspricht. Die Bank erzielte einen Gewinn je verwässerter Aktie von 2,09 US-Dollar, ein Plus von 9,4 % im Jahresvergleich.

Für das erste Halbjahr 2025 erreichte das Nettoergebnis 4,583 Millionen US-Dollar, ein Anstieg von 9,6 % gegenüber dem ersten Halbjahr 2024, mit einem verwässerten Gewinn je Aktie von 4,03 US-Dollar, ein Plus von 8,7 %. Wichtige Leistungskennzahlen sind eine starke Rendite auf das Vermögen von 1,79 % und eine Nettozinsmarge von 4,21 %. Die Gesamtaktiva stiegen auf 530,6 Millionen US-Dollar, die Gesamteinlagen erhöhten sich um 10,7 % auf 470,6 Millionen US-Dollar.

- Record quarterly earnings since bank's 2003 founding

- Net income increased 10.2% to $2.374 million in Q2 2025

- Strong return on assets of 1.79%

- Net interest margin improved to 4.21%

- Total deposits grew 10.7% to $470.6 million

- Nonperforming assets remain low at 0.13% of loans

- Operating expenses increased 23.1% year-over-year

- Salaries and benefits expense rose 31.2%

- Investment securities declined 2.3% year-over-year

FORT WORTH, TX / / July 31, 2025 / Trinity Bank N.A. (OTC PINK:TYBT) today announced operating results for the three months ending June 30, 2025, and YTD results for the six months ending June 30, 2025.

Results of Operations

Trinity Bank, N.A. reported Net Income after Taxes of

For the first six months of 2025, Net Income after Taxes amounted to

Steve Lombardi, Chief Lending Officer, stated, "The second quarter represents record earnings for Trinity Bank and our single best quarter of performance since the Bank was founded in 2003. We are very pleased with the results, which demonstrate the continued success of a business model based on exceptional customer relationships and the strength of the entire Trinity Bank team.

As we move into the second half of the year, we will continue executing on a growth focused strategy, without sacrificing the high credit standards that have made Trinity Bank what it is. Despite some macro-economic uncertainty, primarily related to international trade, the business environment in North Texas remains stable and our customer base remains largely unaffected.

While our outlook for loan growth and credit quality remains positive for the rest of 2025, we are also well positioned to weather any unforeseen storms given our strong liquidity and capital positions."

Page 2 - Trinity Bank Second Quarter 2025

Page 3 - Trinity Bank Second Quarter 2025

Trinity Bank, N.A. is a commercial bank that began operations May 28, 2003. For a full financial statement, visit Trinity Bank's website: Regulatory reporting format is also available at www.fdic.gov.

###

For information contact:

Richard Burt

Executive Vice President

Trinity Bank

817-763-9966

This Press Release may contain certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 regarding future financial conditions, results of operations and the Bank's business operations. Such forward-looking statements involve risks, uncertainties and assumptions, including, but not limited to, monetary policy and general economic conditions in Texas and the greater Dallas-Fort Worth metropolitan area, the risks of changes in interest rates on the level and composition of deposits, loan demand and the values of loan collateral, securities and interest rate protection agreements, the actions of competitors and customers, the success of the Bank in implementing its strategic plan, the failure of the assumptions underlying the reserves for loan losses and the estimations of values of collateral and various financial assets and liabilities, that the costs of technological changes are more difficult or expensive than anticipated, the effects of regulatory restrictions imposed on banks generally, any changes in fiscal, monetary or regulatory policies and other uncertainties as discussed in the Bank's Registration Statement on Form SB��1 filed with the Office of the Comptroller of the Currency. Should one or more of these risks or uncertainties materialize, or should these underlying assumptions prove incorrect, actual outcomes may vary materially from outcomes expected or anticipated by the Bank. A forward-looking statement may include a statement of the assumptions or bases underlying the forward‑looking statement. The Bank believes it has chosen these assumptions or bases in good faith and that they are reasonable. However, the Bank cautions you that assumptions or bases almost always vary from actual results, and the differences between assumptions or bases and actual results can be material. The Bank undertakes no obligation to publicly update or otherwise revise any forward‑looking statements, whether as a result of new information, future events or otherwise, unless the securities laws require the Bank to do so.

TRINITY BANK N.A. | ||||||||||||||||||||||||

(Unaudited) | ||||||||||||||||||||||||

(Dollars in thousands, except per share data) | ||||||||||||||||||||||||

Quarter Ended | Six Months Ending | |||||||||||||||||||||||

June 30 | % | June 30 | % | |||||||||||||||||||||

EARNINGS SUMMARY | 2025 | 2024 | Change | 2025 | 2024 | Change | ||||||||||||||||||

Interest income | $ | 7,455 | $ | 7,107 | 4.9 | % | $ | 14,430 | $ | 14,041 | 2.8 | % | ||||||||||||

Interest expense | 2,295 | 2,713 | -15.4 | % | 4,444 | 5,544 | -19.8 | % | ||||||||||||||||

Net Interest Income | 5,160 | 4,394 | 17.4 | % | 9,986 | 8,497 | 17.5 | % | ||||||||||||||||

Service charges on deposits | 76 | 64 | 18.8 | % | 146 | 120 | 21.6 | % | ||||||||||||||||

Other income | 131 | 121 | 8.3 | % | 238 | 238 | 0.0 | % | ||||||||||||||||

Total Non Interest Income | 207 | 185 | 11.9 | % | 384 | 358 | 7.3 | % | ||||||||||||||||

Salaries and benefits expense | 1,731 | 1,319 | 31.2 | % | 3,239 | 2,541 | 27.5 | % | ||||||||||||||||

Occupancy and equipment expense | 140 | 122 | 14.8 | % | 263 | 244 | 7.8 | % | ||||||||||||||||

Other expense | 712 | 657 | 8.4 | % | 1,526 | 1,277 | 19.5 | % | ||||||||||||||||

Total Non Interest Expense | 2,583 | 2,098 | 23.1 | % | 5,028 | 4,062 | 23.8 | % | ||||||||||||||||

Pretax pre-provision income | 2,784 | 2,481 | 12.2 | % | 5,342 | 4,793 | 11.5 | % | ||||||||||||||||

Gain on sale of Securities | 0 | (4 | ) | N/M | 6 | (4 | ) | N/M | ||||||||||||||||

Gain on sale of Assets | 0 | 36 | N/M | 0 | 53 | N/M | ||||||||||||||||||

Provision for Loan Losses | 0 | 0 | N/M | 0 | 0 | N/M | ||||||||||||||||||

Earnings before income taxes | 2,784 | 2,514 | 10.7 | % | 5,348 | 4,841 | 10.5 | % | ||||||||||||||||

Provision for income taxes | 410 | 360 | 13.9 | % | 765 | 660 | 15.9 | % | ||||||||||||||||

Net Earnings | $ | 2,374 | $ | 2,154 | 10.2 | % | $ | 4,583 | $ | 4,181 | 9.6 | % | ||||||||||||

Basic earnings per share | 2.18 | 2.00 | 2.5 | % | 4.21 | 3.87 | 8.7 | % | ||||||||||||||||

Basic weighted average shares | 1087 | 1,079 | 1088 | 1,079 | ||||||||||||||||||||

outstanding | ||||||||||||||||||||||||

Diluted earnings per share - estimate | 2.09 | 1.91 | 9.4 | % | 4.03 | 3.70 | 8.9 | % | ||||||||||||||||

Diluted weighted average shares outstanding | 1,137 | 1,129 | 1,138 | 1,129 | ||||||||||||||||||||

Average for Quarter | Average for Six Months | |||||||||||||||||||||||

June 30 | % | June 30 | % | |||||||||||||||||||||

BALANCE SHEET SUMMARY | 2025 | 2024 | Change | 2025 | 2024 | Change | ||||||||||||||||||

Total loans | $ | 317,410 | $ | 306,551 | 3.5 | % | $ | 309,931 | $ | 304,424 | 1.8 | % | ||||||||||||

Total short term investments | 66,510 | 25,626 | 159.5 | % | 60,265 | 31,637 | 90.5 | % | ||||||||||||||||

FRB Stock | 459 | 435 | 5.5 | % | 454 | 434 | 4.6 | % | ||||||||||||||||

Total investment securities | 133,949 | 137,088 | -2.3 | % | 135,125 | 139,855 | -3.4 | % | ||||||||||||||||

Earning assets | 518,327 | 469,700 | 10.4 | % | 505,775 | 476,350 | 6.2 | % | ||||||||||||||||

Total assets | 530,621 | 477,700 | 11.1 | % | 517,069 | 483,981 | 6.8 | % | ||||||||||||||||

Noninterest bearing deposits | 137,911 | 131,609 | 4.8 | % | 135,966 | 129,688 | 4.8 | % | ||||||||||||||||

Interest bearing deposits | 332,645 | 293,548 | 13.3 | % | 321,429 | 301,289 | 6.7 | % | ||||||||||||||||

Total deposits | 470,556 | 425,157 | 10.7 | % | 457,395 | 430,977 | 6.1 | % | ||||||||||||||||

Fed Funds Purchased and Repurchase Agreements | 0 | 0 | N/M | 0 | 0 | N/M | ||||||||||||||||||

Shareholders' equity | $ | 62,680 | $ | 54,951 | 14.1 | % | $ | 61,767 | $ | 54,437 | 13.5 | % | ||||||||||||

TRINITY BANK N.A. | ||||||||||||||||||||

(Unaudited) | ||||||||||||||||||||

(Dollars in thousands, except per share data) | ||||||||||||||||||||

Average for Quarter Ending | ||||||||||||||||||||

June 30, | March 31, | Dec 31, | Sep 30, | June 30, | ||||||||||||||||

BALANCE SHEET SUMMARY | 2025 | 2025 | 2024 | 2024 | 2024 | |||||||||||||||

Total loans | $ | 317,410 | $ | 302,369 | $ | 297,595 | $ | 300,487 | $ | 306,551 | ||||||||||

Total short term investments | 66,510 | 53,950 | 84,667 | 38,112 | 25,626 | |||||||||||||||

FRB Stock | 459 | 449 | 438 | 437 | 435 | |||||||||||||||

Total investment securities | 133,949 | 136,314 | 139,200 | 137,751 | 137,088 | |||||||||||||||

Earning assets | 518,327 | 493,082 | 521,900 | 476,787 | 469,700 | |||||||||||||||

Total assets | 530,621 | 503,366 | 529,766 | 485,034 | 477,700 | |||||||||||||||

Noninterest bearing deposits | 137,911 | 133,982 | 140,237 | 131,659 | 131,609 | |||||||||||||||

Interest bearing deposits | 332,645 | 310,105 | 331,293 | 297,480 | 293,548 | |||||||||||||||

Total deposits | 470,556 | 444,087 | 471,529 | 429,139 | 425,157 | |||||||||||||||

Fed Funds Purchased and Repurchase Agreements | 0 | 0 | 0 | 0 | 0 | |||||||||||||||

Shareholders' equity | $ | 62,680 | $ | 60,843 | $ | 58,388 | $ | 56,857 | $ | 54,951 | ||||||||||

Quarter Ended | ||||||||||||||||||||

June 30, | March 31, | Dec 31, | Sep 30, | June 30, | ||||||||||||||||

HISTORICAL EARNINGS SUMMARY | 2025 | 2025 | 2024 | 2024 | 2024 | |||||||||||||||

Interest income | $ | 7,455 | $ | 6,975 | $ | 7,426 | $ | 7,112 | $ | 7,107 | ||||||||||

Interest expense | 2,295 | 2,149 | 2,681 | 2,749 | 2,713 | |||||||||||||||

Net Interest Income | 5,160 | 4,826 | 4,745 | 4,363 | 4,394 | |||||||||||||||

Service charges on deposits | 76 | 71 | 70 | 65 | 64 | |||||||||||||||

Other income | 131 | 106 | 112 | 109 | 121 | |||||||||||||||

Total Non Interest Income | 207 | 177 | 182 | 174 | 185 | |||||||||||||||

Salaries and benefits expense | 1,731 | 1,508 | 1,343 | 1,368 | 1,319 | |||||||||||||||

Occupancy and equipment expense | 140 | 123 | 117 | 133 | 122 | |||||||||||||||

Other expense | 712 | 814 | 575 | 601 | 657 | |||||||||||||||

Total Non Interest Expense | 2,583 | 2,445 | 2,035 | 2,102 | 2,098 | |||||||||||||||

Pretax pre-provision income | 2,784 | 2,558 | 2,892 | 2,435 | 2,481 | |||||||||||||||

Gain on sale of securities | 0 | 6 | 1 | 4 | (4 | ) | ||||||||||||||

Gain on sale of Other Assets | 0 | 0 | 0 | 0 | 36 | |||||||||||||||

Provision for Loan Losses | 0 | 0 | 350 | 0 | 0 | |||||||||||||||

Earnings before income taxes | 2,784 | 2,564 | 2,543 | 2,439 | 2,514 | |||||||||||||||

Provision for income taxes | 410 | 355 | 365 | 340 | 360 | |||||||||||||||

Net Earnings | $ | 2,374 | $ | 2,209 | $ | 2,178 | $ | 2,099 | $ | 2,154 | ||||||||||

Diluted earnings per share | $ | 2.09 | $ | 1.94 | $ | 1.92 | $ | 1.86 | $ | 1.91 | ||||||||||

TRINITY BANK N.A. | ||||||||||||||||||||

(Unaudited) | ||||||||||||||||||||

(Dollars in thousands, except per share data) | ||||||||||||||||||||

Ending Balance | ||||||||||||||||||||

June 30, | March 31, | Dec. 31, | Sept. 30, | June 30, | ||||||||||||||||

HISTORICAL BALANCE SHEET | 2025 | 2025 | 2024 | 2024 | 2024 | |||||||||||||||

Total loans | $ | 325,809 | $ | 304,944 | $ | 305,864 | $ | 296,906 | $ | 304,810 | ||||||||||

FRB Stock | 461 | 456 | 439 | 438 | 435 | |||||||||||||||

Total short term investments | 55,130 | 90,040 | 69,746 | 59,576 | 10,003 | |||||||||||||||

Total investment securities | 132,989 | 124,619 | 138,306 | 137,510 | 136,331 | |||||||||||||||

Total earning assets | 514,389 | 520,059 | 514,355 | 494,430 | 451,579 | |||||||||||||||

Allowance for loan losses | (5,589 | ) | (5,586 | ) | (5,583 | ) | (5,230 | ) | (5,227 | ) | ||||||||||

Premises and equipment | 4,079 | 4,044 | 4,123 | 2,393 | 2,397 | |||||||||||||||

Other Assets | 14,296 | 10,297 | 9,339 | 9,739 | 14,276 | |||||||||||||||

Total assets | 527,175 | 528,814 | 522,234 | 501,332 | 463,025 | |||||||||||||||

Noninterest bearing deposits | 133,902 | 140,500 | 146,834 | 137,594 | 128,318 | |||||||||||||||

Interest bearing deposits | 331,050 | 329,329 | 318,206 | 305,010 | 280,945 | |||||||||||||||

Total deposits | 464,952 | 469,829 | 465,040 | 442,604 | 409,263 | |||||||||||||||

Fed Funds Purchased and Repurchase Agreements | 0 | 0 | 0 | 0 | 0 | |||||||||||||||

Other Liabilities | 3,072 | 2,661 | 2,711 | 2,901 | 2,804 | |||||||||||||||

Total liabilities | 468,024 | 472,490 | 467,751 | 445,505 | 412,067 | |||||||||||||||

Shareholders' Equity Actual | 63,664 | 62,276 | 59,758 | 57,976 | 55,915 | |||||||||||||||

Unrealized Gain/Loss - AFS | (4,513 | ) | (5,952 | ) | (5,275 | ) | (2,149 | ) | (4,957 | ) | ||||||||||

Total Equity | $ | 59,151 | $ | 56,324 | $ | 54,483 | $ | 55,827 | $ | 50,958 | ||||||||||

Quarter Ending | ||||||||||||||||||||

June 30, | March 31, | Dec. 31, | Sept. 30, | June 30, | ||||||||||||||||

NONPERFORMING ASSETS | 2025 | 2025 | 2024 | 2024 | 2024 | |||||||||||||||

Nonaccrual loans | $ | 424 | $ | 949 | $ | 1,047 | $ | 0 | $ | 0 | ||||||||||

Restructured loans | 0 | 0 | 0 | 505 | 552 | |||||||||||||||

Other real estate & foreclosed assets | 0 | 0 | 0 | 0 | 0 | |||||||||||||||

Accruing loans past due 90 days or more | 0 | 0 | 0 | 0 | 0 | |||||||||||||||

Total nonperforming assets | $ | 424 | $ | 949 | $ | 1,047 | $ | 505 | $ | 552 | ||||||||||

Accruing loans past due 30-89 days | $ | 0 | $ | 1,000 | $ | 0 | $ | 39 | $ | 1,274 | ||||||||||

Total nonperforming assets as a percentage | ||||||||||||||||||||

of loans and foreclosed assets | 0.13 | % | 0.31 | % | 0.34 | % | 0.17 | % | 0.18 | % | ||||||||||

TRINITY BANK N.A. | ||||||||||||||||||||

(Unaudited) | ||||||||||||||||||||

(Dollars in thousands, except per share data) | ||||||||||||||||||||

Quarter Ending | ||||||||||||||||||||

ALLOWANCE FOR | June 30, | March 31, | Dec. 31, | Sept. 30, | June 30, | |||||||||||||||

LOAN LOSSES | 2025 | 2025 | 2024 | 2024 | 2024 | |||||||||||||||

Balance at beginning of period | $ | 5,586 | $ | 5,583 | $ | 5,230 | $ | 5,227 | $ | 5,224 | ||||||||||

Loans charged off | 0 | 0 | 0 | 0 | 0 | |||||||||||||||

Loan recoveries | 3 | 3 | 3 | 3 | 3 | |||||||||||||||

Net (charge-offs) recoveries | 3 | 3 | 3 | 3 | 3 | |||||||||||||||

Provision for loan losses | 0 | 0 | 350 | 0 | 0 | |||||||||||||||

Balance at end of period | $ | 5,589 | $ | 5,586 | $ | 5,583 | $ | 5,230 | $ | 5,227 | ||||||||||

Allowance for loan losses | ||||||||||||||||||||

as a percentage of total loans | 1.72 | % | 1.83 | % | 1.83 | % | 1.76 | % | 1.71 | % | ||||||||||

Allowance for loan losses | ||||||||||||||||||||

as a percentage of nonperforming assets | 1318 | % | 589 | % | 533 | % | 1036 | % | 947 | % | ||||||||||

Net charge-offs (recoveries) as a | ||||||||||||||||||||

percentage of average loans | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | ||||||||||

Provision for loan losses | ||||||||||||||||||||

as a percentage of average loans | 0.00 | % | 0.00 | % | 0.11 | % | 0.00 | % | 0.00 | % | ||||||||||

Quarter Ending | ||||||||||||||||||||

June 30, | March 31, | Dec. 31, | Sept. 30, | June 30, | ||||||||||||||||

SELECTED RATIOS | 2025 | 2025 | 2024 | 2024 | 2024 | |||||||||||||||

Return on average assets (annualized) | 1.79 | % | 1.76 | % | 1.64 | % | 1.73 | % | 1.80 | % | ||||||||||

Return on average equity (annualized) | 16.69 | % | 15.67 | % | 15.85 | % | 15.91 | % | 17.42 | % | ||||||||||

Return on average equity (excluding unrealized gain on investments) | 15.15 | % | 14.52 | % | 14.92 | % | 14.77 | % | 15.68 | % | ||||||||||

Average shareholders' equity to average assets | 11.81 | % | 12.09 | % | 11.02 | % | 11.72 | % | 11.50 | % | ||||||||||

Yield on earning assets (tax equivalent) | 5.98 | % | 5.72 | % | 5.92 | % | 6.20 | % | 6.28 | % | ||||||||||

Effective Cost of Funds | 1.77 | % | 1.75 | % | 2.06 | % | 2.31 | % | 2.31 | % | ||||||||||

Net interest margin (tax equivalent) | 4.21 | % | 3.97 | % | 3.86 | % | 3.89 | % | 3.97 | % | ||||||||||

Efficiency ratio (tax equivalent) | 45.6 | % | 46.2 | % | 39.0 | % | 43.7 | % | 43.2 | % | ||||||||||

End of period book value per common share | $ | 54.42 | $ | 51.82 | $ | 50.21 | $ | 51.79 | $ | 47.23 | ||||||||||

End of period book value (excluding unrealized gain/loss on investments) | $ | 58.57 | $ | 57.29 | $ | 55.08 | $ | 53.78 | $ | 51.82 | ||||||||||

End of period common shares outstanding (in 000's) | 1,087 | 1,087 | 1,085 | 1,078 | 1,079 | |||||||||||||||

TRINITY BANK N.A. | |||||||||||||||||||||||||||||||||

(Unaudited) | |||||||||||||||||||||||||||||||||

(Dollars in thousands, except per share data) | |||||||||||||||||||||||||||||||||

Three Months Ending | |||||||||||||||||||||||||||||||||

June 30, 2025 | June 30, 2024 | ||||||||||||||||||||||||||||||||

Tax | Tax | ||||||||||||||||||||||||||||||||

Average | Equivalent | Average | Equivalent | ||||||||||||||||||||||||||||||

YIELD ANALYSIS | Balance | Interest | Yield | Yield | Balance | Interest | Yield | Yield | |||||||||||||||||||||||||

Interest Earning Assets: | |||||||||||||||||||||||||||||||||

Short term investment | $ | 66,510 | $ | 740 | 4.45 | % | 4.45 | % | $ | 25,626 | $ | 356 | 5.56 | % | 5.56 | % | |||||||||||||||||

FRB Stock | 459 | 7 | 6.00 | % | 6.00 | % | 435 | 6 | 6.00 | % | 6.00 | % | |||||||||||||||||||||

Taxable securities | 4,944 | 52 | 4.21 | % | 4.21 | % | 495 | 6 | 4.85 | % | 4.85 | % | |||||||||||||||||||||

Tax Free securities | 129,005 | 1,111 | 3.44 | % | 4.36 | % | 136,593 | 1,234 | 3.61 | % | 4.41 | % | |||||||||||||||||||||

Loans | 317,409 | 5,545 | 6.99 | % | 6.99 | % | 306,551 | 5,504 | 7.18 | % | 7.18 | % | |||||||||||||||||||||

Total Interest Earning Assets | 518,327 | 7,455 | 5.75 | % | 5.98 | % | 469,700 | 7,106 | 6.05 | % | 6.28 | % | |||||||||||||||||||||

Noninterest Earning Assets: | |||||||||||||||||||||||||||||||||

Cash and due from banks | 6,199 | 5,791 | |||||||||||||||||||||||||||||||

Other assets | 11,683 | 7,436 | |||||||||||||||||||||||||||||||

Allowance for loan losses | (5,588 | ) | (5,227 | ) | |||||||||||||||||||||||||||||

Total Noninterest Earning Assets | 12,294 | 8,000 | |||||||||||||||||||||||||||||||

Total Assets | $ | 530,621 | $ | 477,700 | |||||||||||||||||||||||||||||

Interest Bearing Liabilities: | |||||||||||||||||||||||||||||||||

Transaction and Money Market accounts | $ | 216,131 | $ | 1,165 | 2.16 | % | 2.16 | % | 190,542 | $ | 1,522 | 3.20 | % | 3.20 | % | ||||||||||||||||||

Certificates and other time deposits | 116,430 | 1,130 | 3.88 | % | 3.88 | % | 103,006 | 1,191 | 4.62 | % | 4.62 | % | |||||||||||||||||||||

Other borrowings | 0 | 0 | 0.00 | % | 0.00 | % | 0 | 0 | 0.00 | % | 0.00 | % | |||||||||||||||||||||

Total Interest Bearing Liabilities | 332,561 | 2,295 | 2.76 | % | 2.76 | % | 293,548 | 2,713 | 3.70 | % | 3.70 | % | |||||||||||||||||||||

Noninterest Bearing Liabilities: | |||||||||||||||||||||||||||||||||

Demand deposits | 137,995 | 131,609 | |||||||||||||||||||||||||||||||

Other liabilities | 3,154 | 3,069 | |||||||||||||||||||||||||||||||

Shareholders' Equity | 56,911 | 49,474 | |||||||||||||||||||||||||||||||

Total Liabilities and Shareholders Equity | $ | 530,621 | $ | 477,700 | |||||||||||||||||||||||||||||

Net Interest Income and Spread | $ | 185,766 | $ | 5,160 | 2.99 | % | 3.22 | % | 176,152 | $ | 4,393 | 2.35 | % | 2.59 | % | ||||||||||||||||||

Net Interest Margin | 3.98 | % | 4.21 | % | 3.74 | % | 3.97 | % | |||||||||||||||||||||||||

TRINITY BANK N.A. | ||||||||||||||||

(Unaudited) | ||||||||||||||||

(Dollars in thousands, except per share data) | ||||||||||||||||

June 30 | June 30 | |||||||||||||||

2025 | % | 2024 | % | |||||||||||||

LOAN PORTFOLIO | ||||||||||||||||

Commercial and industrial | $ | 164,845 | 50.60 | % | $ | 164,397 | 53.93 | % | ||||||||

AG���˹ٷ� estate: | ||||||||||||||||

Commercial | 109,089 | 33.48 | % | 96,074 | 31.52 | % | ||||||||||

Residential | 13,100 | 4.02 | % | 16,263 | 5.34 | % | ||||||||||

Construction and development | 38,427 | 11.79 | % | 27,722 | 9.09 | % | ||||||||||

Consumer | 348 | 0.11 | % | 354 | 0.12 | % | ||||||||||

Total loans | $ | 325,809 | 100.00 | % | 304,810 | 100.00 | % | |||||||||

June 30 | June 30 | |||||||

2025 | 2024 | |||||||

REGULATORY CAPITAL DATA | ||||||||

Tier 1 Capital | $ | 63,663 | $ | 55,914 | ||||

Total Capital (Tier 1 + Tier 2) | $ | 66,622 | $ | 60,247 | ||||

Total Risk-Adjusted Assets | $ | 346,179 | $ | 345,039 | ||||

Tier 1 Risk-Based Capital Ratio | 17.99 | % | 16.21 | % | ||||

Total Risk-Based Capital Ratio | 19.25 | % | 17.46 | % | ||||

Tier 1 Leverage Ratio | 12.37 | % | 11.70 | % | ||||

OTHER DATA | ||||||||

Full Time Equivalent | ||||||||

Employees (FTE's) | 31 | 29 | ||||||

Stock Price Range | ||||||||

(For the Three Months Ended): | ||||||||

High | $ | 87.50 | $ | 94.00 | ||||

Low | $ | 86.50 | $ | 86.75 | ||||

Close | $ | 87.00 | $ | 89.75 | ||||

SOURCE: Trinity Bank, NA (Fort Worth, Texas)

View the original on ACCESS Newswire