[6-K] UBS Group AG Current Report (Foreign Issuer)

UBS’s Q2-25 Form 6-K combines solid operating momentum with a forceful warning on Swiss capital reforms. Management reports that extreme market volatility in April did not derail performance: underlying return on CET1 capital reached 13.3 % for 1H-25, Group invested assets hit a record US$6.6 tn, and private/institutional client activity was strong across regions. UBS granted or renewed CHF40 bn of loans, underscoring its role in the Swiss economy. Credit Suisse integration execution risk continues to fall: all clients booked outside Switzerland have migrated and the first Swiss wave is complete.

CEO Sergio Ermotti devotes much of the remarks to the Swiss Federal Council’s 6 Jun 25 banking-reform proposals. UBS supports most measures but “strongly disagrees�� with the capital package. Removal of Credit Suisse concessions plus size-based surcharges already oblige UBS to raise ��US$18 bn; the new rules would demand a further US$24 bn, lifting the total required increase to US$42 bn. The resulting de-facto minimum CET1 ratio would be at least 50 % higher than the G-SIB average, which UBS deems neither proportionate nor internationally aligned. Management argues higher capital would raise funding costs, constrain services, and harm Swiss households and businesses. UBS will continue to engage policymakers but stresses its fiduciary duty to protect shareholders.

Il modulo 6-K di UBS per il secondo trimestre 2025 unisce un solido slancio operativo a un forte avvertimento sulle riforme del capitale svizzero. La direzione riferisce che l’estrema volatilità dei mercati in aprile non ha compromesso le performance: il rendimento sottostante sul capitale CET1 ha raggiunto il 13,3% per il primo semestre 2025, gli asset investiti del Gruppo hanno toccato un record di 6,6 trilioni di dollari USA e l’attività dei clienti privati e istituzionali è stata intensa in tutte le regioni. UBS ha concesso o rinnovato prestiti per 40 miliardi di franchi svizzeri, sottolineando il suo ruolo nell’economia svizzera. Il rischio di esecuzione dell’integrazione di Credit Suisse continua a diminuire: tutti i clienti registrati fuori dalla Svizzera sono stati trasferiti e la prima fase in Svizzera è completata.

Il CEO Sergio Ermotti dedica gran parte del suo intervento alle proposte di riforma bancaria del Consiglio federale svizzero del 6 giugno 2025. UBS sostiene la maggior parte delle misure ma è in forte disaccordo con il pacchetto sul capitale. La rimozione delle concessioni a Credit Suisse più le maggiorazioni basate sulle dimensioni obbligano già UBS a raccogliere circa 18 miliardi di dollari USA; le nuove regole richiederebbero ulteriori 24 miliardi di dollari, portando l’aumento totale richiesto a 42 miliardi di dollari. Il rapporto CET1 minimo di fatto risulterebbe almeno del 50% superiore alla media dei G-SIB, cosa che UBS considera né proporzionata né allineata a livello internazionale. La direzione sostiene che un capitale più elevato aumenterebbe i costi di finanziamento, limiterebbe i servizi e danneggerebbe famiglie e imprese svizzere. UBS continuerà a dialogare con i decisori politici ma sottolinea il suo dovere fiduciario di proteggere gli azionisti.

El Formulario 6-K de UBS para el segundo trimestre de 2025 combina un sólido impulso operativo con una contundente advertencia sobre las reformas de capital suizas. La dirección informa que la extrema volatilidad del mercado en abril no afectó el desempeño: el rendimiento subyacente sobre el capital CET1 alcanzó un 13,3 % en el primer semestre de 2025, los activos invertidos del Grupo alcanzaron un récord de 6,6 billones de dólares estadounidenses, y la actividad de clientes privados e institucionales fue fuerte en todas las regiones. UBS concedió o renovó préstamos por 40 mil millones de francos suizos, destacando su papel en la economía suiza. El riesgo de ejecución de la integración de Credit Suisse sigue disminuyendo: todos los clientes registrados fuera de Suiza han sido migrados y la primera fase en Suiza está completa.

El CEO Sergio Ermotti dedica gran parte de sus comentarios a las propuestas de reforma bancaria del Consejo Federal Suizo del 6 de junio de 2025. UBS apoya la mayoría de las medidas pero “discrepa firmemente�� con el paquete de capital. La eliminación de las concesiones de Credit Suisse más los recargos basados en el tamaño ya obligan a UBS a aumentar aproximadamente 18 mil millones de dólares; las nuevas reglas exigirían otros 24 mil millones de dólares, elevando el aumento total requerido a 42 mil millones de dólares. La ratio mínima de CET1 resultante sería al menos un 50 % superior al promedio de los G-SIB, lo que UBS considera ni proporcional ni alineado internacionalmente. La dirección argumenta que un mayor capital aumentaría los costos de financiamiento, limitaría los servicios y perjudicaría a los hogares y empresas suizas. UBS continuará dialogando con los responsables políticos pero enfatiza su deber fiduciario de proteger a los accionistas.

UBS�� 2025�� 2분기 Form 6-K�� 견고�� 운영 모멘텀�� 스위�� 자본 개혁�� 대�� 강력�� 경고�� 결합하고 있습니다. 경영진은 4월의 극심�� 시장 변동성에도 불구하고 성과가 흔들리지 않았다고 보고합니��: 기초 CET1 자본 수익률은 2025�� 상반�� 13.3%�� 도달했으��, 그룹 투자 자산은 역대 최고�� 6.6�� 달러�� 기록했고, 개인 �� 기관 고객 활동은 �� 지역에�� 강세�� 보였습니��. UBS�� 400�� 스위�� 프랑�� 대출을 신규 승인하거�� 갱신하며 스위�� 경제 �� 역할�� 강조했습니다. 크레디트 스위�� 통합 실행 위험은 계속 감소 중이��, 스위�� 외부�� 등록�� 모든 고객�� 이전 완료되었�� �� 번째 스위�� 단계�� 마무리되었습니다.

CEO 세르지�� 에르모티�� 2025�� 6�� 6�� 스위�� 연방평의회의 은�� 개혁 제안�� 대�� 많은 부분을 할애했습니다. UBS�� 대부분의 조치�� 지지하지�� 자본 패키지에는 강력�� 반대합니��. 크레디트 스위�� 특혜 제거와 규모 기반 추가 부담금으로 이미 UBS�� �� 180�� 달러�� 증자해야 하며, �� 규칙은 추가 240�� 달러�� 요구�� �� 증자 규모가 420�� 달러�� 이르�� 됩니��. 결과적으�� 최소 CET1 비율은 G-SIB 평균보다 최소 50% 이상 높아�� ��으로, UBS�� 이를 비례적이지 않고 국제 기준에도 맞지 않는다고 보고 있습니다. 경영진은 자본 증가가 자금 조달 비용�� 높이�� 서비�� 제공�� 제한하며 스위�� 가계와 기업�� 피해�� �� 것이라고 주장합니��. UBS�� 정책 입안자와 계속 협의�� 것이�� 주주 보호라는 신탁 의무�� 강조합니��.

Le formulaire 6-K d’UBS pour le deuxième trimestre 2025 allie un solide élan opérationnel à un avertissement ferme concernant les réformes du capital en Suisse. La direction rapporte que la volatilité extrême des marchés en avril n’a pas entravé la performance : le rendement sous-jacent du capital CET1 a atteint 13,3 % pour le premier semestre 2025, les actifs investis du groupe ont atteint un record de 6,6 billions de dollars US, et l’activité des clients privés et institutionnels a été soutenue dans toutes les régions. UBS a accordé ou renouvelé des prêts pour 40 milliards de francs suisses, soulignant ainsi son rôle dans l’économie suisse. Le risque d’exécution de l’intégration de Credit Suisse continue de diminuer : tous les clients enregistrés hors de Suisse ont été migrés et la première phase en Suisse est terminée.

Le PDG Sergio Ermotti consacre une grande partie de ses remarques aux propositions de réforme bancaire du Conseil fédéral suisse du 6 juin 2025. UBS soutient la plupart des mesures mais « désapprouve fermement » le paquet sur le capital. La suppression des concessions de Credit Suisse ainsi que les surcharges basées sur la taille obligent déjà UBS à augmenter d’environ 18 milliards de dollars US ; les nouvelles règles exigeraient un supplément de 24 milliards de dollars US, portant l’augmentation totale requise à 42 milliards de dollars US. Le ratio CET1 minimum de facto serait au moins 50 % supérieur à la moyenne des G-SIB, ce que UBS juge ni proportionné ni aligné internationalement. La direction soutient qu’un capital plus élevé augmenterait les coûts de financement, limiterait les services et nuirait aux ménages et entreprises suisses. UBS continuera à dialoguer avec les décideurs politiques mais souligne son devoir fiduciaire de protéger les actionnaires.

UBS�� Form 6-K für das zweite Quartal 2025 kombiniert ein solides operatives Momentum mit einer deutlichen Warnung vor den Schweizer Kapitalreformen. Das Management berichtet, dass die extreme Marktvolatilität im April die Performance nicht beeinträchtigte: Die zugrundeliegende Rendite auf das CET1-Kapital erreichte 13,3 % für das erste Halbjahr 2025, die vom Konzern verwalteten Vermögenswerte erreichten mit 6,6 Billionen US-Dollar einen Rekord, und die Aktivitäten der Privat- und institutionellen Kunden waren in allen Regionen stark. UBS gewährte oder verlängerte Kredite in Höhe von 40 Milliarden Schweizer Franken und unterstreicht damit seine Rolle in der Schweizer Wirtschaft. Das Risiko bei der Integration von Credit Suisse sinkt weiter: Alle außerhalb der Schweiz gebuchten Kunden wurden migriert, und die erste Schweizer Welle ist abgeschlossen.

CEO Sergio Ermotti widmet einen Großteil seiner Ausführungen den Bankenreformvorschlägen des Schweizer Bundesrates vom 6. Juni 2025. UBS unterstützt die meisten Maßnahmen, ist jedoch mit dem Kapitalpaket stark nicht einverstanden. Der Wegfall der Konzessionen von Credit Suisse sowie größenabhängige Zuschläge zwingen UBS bereits, etwa 18 Milliarden US-Dollar zusätzliches Kapital aufzubringen; die neuen Regeln würden weitere 24 Milliarden US-Dollar erfordern, womit die insgesamt geforderte Erhöhung 42 Milliarden US-Dollar beträgt. Die daraus resultierende de-facto Mindest-CET1-Quote läge mindestens 50 % über dem Durchschnitt der G-SIBs, was UBS weder für verhältnismäßig noch international abgestimmt hält. Das Management argumentiert, dass höheres Kapital die Finanzierungskosten erhöhen, Dienstleistungen einschränken und Schweizer Haushalte sowie Unternehmen schädigen würde. UBS wird weiterhin mit den politischen Entscheidungsträgern im Gespräch bleiben, betont jedoch seine treuhänderische Pflicht zum Schutz der Aktionäre.

- 13.3 % underlying return on CET1 capital for 1H-25 indicates strong profitability.

- Group invested assets reached a record US$6.6 tn, signalling effective client retention and growth.

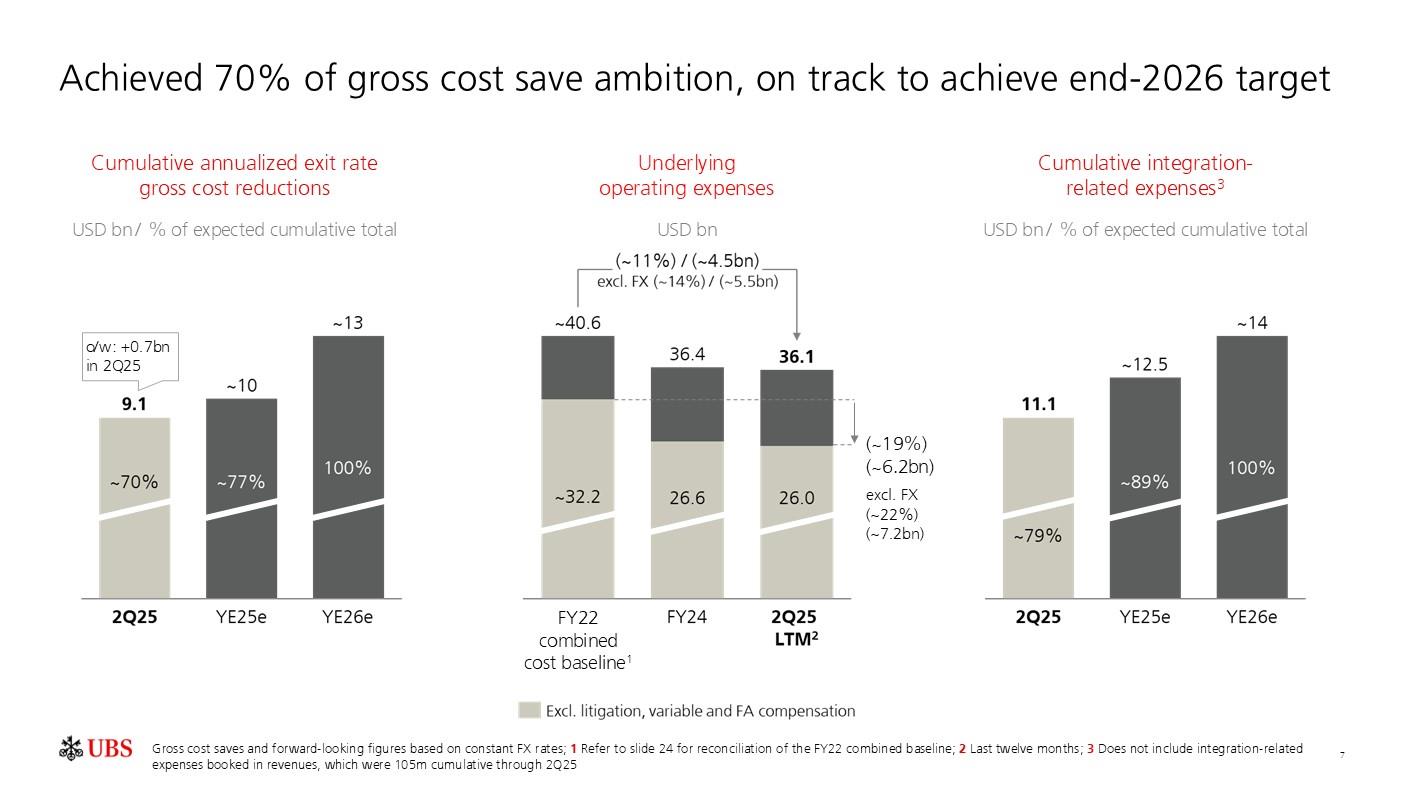

- Credit Suisse integration milestones met, reducing execution risk and supporting synergy realization.

- Granted/renewed CHF40 bn in Swiss loans, reinforcing domestic franchise strength.

- Swiss capital proposals could force UBS to raise an additional US$24 bn, totalling US$42 bn of extra capital and potentially diluting returns.

- Resulting de-facto minimum CET1 ratio would be ��50 % higher than G-SIB peers, threatening competitiveness.

- Management focus on regulatory lobbying highlights elevated policy risk for investors.

Insights

TL;DR �� Strong 1H returns offset by potentially onerous US$42 bn capital overhang; net investor impact neutral-to-slightly negative.

The filing confirms resilient fundamentals: 13.3 % CET1 RoC, record US$6.6 tn assets, and smooth Credit Suisse migration support the equity story. However, the Swiss reform could dilute ROE, limit buybacks, and hamper growth if US$24 bn incremental capital is enforced. Until regulatory clarity emerges, upside is capped despite solid execution.

TL;DR �� Proposed Swiss rules would make UBS an outlier, raising systemic capital >50 % above peers.

UBS frames the capital plan as extreme versus EU/UK/US regimes, highlighting misalignment and economic spill-overs. If enacted, the bank’s strategic flexibility and dividend capacity face material pressure. Still, management’s early public pushback suggests lobbying could soften the final framework. Impactful but not yet determinative.

Il modulo 6-K di UBS per il secondo trimestre 2025 unisce un solido slancio operativo a un forte avvertimento sulle riforme del capitale svizzero. La direzione riferisce che l’estrema volatilità dei mercati in aprile non ha compromesso le performance: il rendimento sottostante sul capitale CET1 ha raggiunto il 13,3% per il primo semestre 2025, gli asset investiti del Gruppo hanno toccato un record di 6,6 trilioni di dollari USA e l’attività dei clienti privati e istituzionali è stata intensa in tutte le regioni. UBS ha concesso o rinnovato prestiti per 40 miliardi di franchi svizzeri, sottolineando il suo ruolo nell’economia svizzera. Il rischio di esecuzione dell’integrazione di Credit Suisse continua a diminuire: tutti i clienti registrati fuori dalla Svizzera sono stati trasferiti e la prima fase in Svizzera è completata.

Il CEO Sergio Ermotti dedica gran parte del suo intervento alle proposte di riforma bancaria del Consiglio federale svizzero del 6 giugno 2025. UBS sostiene la maggior parte delle misure ma è in forte disaccordo con il pacchetto sul capitale. La rimozione delle concessioni a Credit Suisse più le maggiorazioni basate sulle dimensioni obbligano già UBS a raccogliere circa 18 miliardi di dollari USA; le nuove regole richiederebbero ulteriori 24 miliardi di dollari, portando l’aumento totale richiesto a 42 miliardi di dollari. Il rapporto CET1 minimo di fatto risulterebbe almeno del 50% superiore alla media dei G-SIB, cosa che UBS considera né proporzionata né allineata a livello internazionale. La direzione sostiene che un capitale più elevato aumenterebbe i costi di finanziamento, limiterebbe i servizi e danneggerebbe famiglie e imprese svizzere. UBS continuerà a dialogare con i decisori politici ma sottolinea il suo dovere fiduciario di proteggere gli azionisti.

El Formulario 6-K de UBS para el segundo trimestre de 2025 combina un sólido impulso operativo con una contundente advertencia sobre las reformas de capital suizas. La dirección informa que la extrema volatilidad del mercado en abril no afectó el desempeño: el rendimiento subyacente sobre el capital CET1 alcanzó un 13,3 % en el primer semestre de 2025, los activos invertidos del Grupo alcanzaron un récord de 6,6 billones de dólares estadounidenses, y la actividad de clientes privados e institucionales fue fuerte en todas las regiones. UBS concedió o renovó préstamos por 40 mil millones de francos suizos, destacando su papel en la economía suiza. El riesgo de ejecución de la integración de Credit Suisse sigue disminuyendo: todos los clientes registrados fuera de Suiza han sido migrados y la primera fase en Suiza está completa.

El CEO Sergio Ermotti dedica gran parte de sus comentarios a las propuestas de reforma bancaria del Consejo Federal Suizo del 6 de junio de 2025. UBS apoya la mayoría de las medidas pero “discrepa firmemente�� con el paquete de capital. La eliminación de las concesiones de Credit Suisse más los recargos basados en el tamaño ya obligan a UBS a aumentar aproximadamente 18 mil millones de dólares; las nuevas reglas exigirían otros 24 mil millones de dólares, elevando el aumento total requerido a 42 mil millones de dólares. La ratio mínima de CET1 resultante sería al menos un 50 % superior al promedio de los G-SIB, lo que UBS considera ni proporcional ni alineado internacionalmente. La dirección argumenta que un mayor capital aumentaría los costos de financiamiento, limitaría los servicios y perjudicaría a los hogares y empresas suizas. UBS continuará dialogando con los responsables políticos pero enfatiza su deber fiduciario de proteger a los accionistas.

UBS�� 2025�� 2분기 Form 6-K�� 견고�� 운영 모멘텀�� 스위�� 자본 개혁�� 대�� 강력�� 경고�� 결합하고 있습니다. 경영진은 4월의 극심�� 시장 변동성에도 불구하고 성과가 흔들리지 않았다고 보고합니��: 기초 CET1 자본 수익률은 2025�� 상반�� 13.3%�� 도달했으��, 그룹 투자 자산은 역대 최고�� 6.6�� 달러�� 기록했고, 개인 �� 기관 고객 활동은 �� 지역에�� 강세�� 보였습니��. UBS�� 400�� 스위�� 프랑�� 대출을 신규 승인하거�� 갱신하며 스위�� 경제 �� 역할�� 강조했습니다. 크레디트 스위�� 통합 실행 위험은 계속 감소 중이��, 스위�� 외부�� 등록�� 모든 고객�� 이전 완료되었�� �� 번째 스위�� 단계�� 마무리되었습니다.

CEO 세르지�� 에르모티�� 2025�� 6�� 6�� 스위�� 연방평의회의 은�� 개혁 제안�� 대�� 많은 부분을 할애했습니다. UBS�� 대부분의 조치�� 지지하지�� 자본 패키지에는 강력�� 반대합니��. 크레디트 스위�� 특혜 제거와 규모 기반 추가 부담금으로 이미 UBS�� �� 180�� 달러�� 증자해야 하며, �� 규칙은 추가 240�� 달러�� 요구�� �� 증자 규모가 420�� 달러�� 이르�� 됩니��. 결과적으�� 최소 CET1 비율은 G-SIB 평균보다 최소 50% 이상 높아�� ��으로, UBS�� 이를 비례적이지 않고 국제 기준에도 맞지 않는다고 보고 있습니다. 경영진은 자본 증가가 자금 조달 비용�� 높이�� 서비�� 제공�� 제한하며 스위�� 가계와 기업�� 피해�� �� 것이라고 주장합니��. UBS�� 정책 입안자와 계속 협의�� 것이�� 주주 보호라는 신탁 의무�� 강조합니��.

Le formulaire 6-K d’UBS pour le deuxième trimestre 2025 allie un solide élan opérationnel à un avertissement ferme concernant les réformes du capital en Suisse. La direction rapporte que la volatilité extrême des marchés en avril n’a pas entravé la performance : le rendement sous-jacent du capital CET1 a atteint 13,3 % pour le premier semestre 2025, les actifs investis du groupe ont atteint un record de 6,6 billions de dollars US, et l’activité des clients privés et institutionnels a été soutenue dans toutes les régions. UBS a accordé ou renouvelé des prêts pour 40 milliards de francs suisses, soulignant ainsi son rôle dans l’économie suisse. Le risque d’exécution de l’intégration de Credit Suisse continue de diminuer : tous les clients enregistrés hors de Suisse ont été migrés et la première phase en Suisse est terminée.

Le PDG Sergio Ermotti consacre une grande partie de ses remarques aux propositions de réforme bancaire du Conseil fédéral suisse du 6 juin 2025. UBS soutient la plupart des mesures mais « désapprouve fermement » le paquet sur le capital. La suppression des concessions de Credit Suisse ainsi que les surcharges basées sur la taille obligent déjà UBS à augmenter d’environ 18 milliards de dollars US ; les nouvelles règles exigeraient un supplément de 24 milliards de dollars US, portant l’augmentation totale requise à 42 milliards de dollars US. Le ratio CET1 minimum de facto serait au moins 50 % supérieur à la moyenne des G-SIB, ce que UBS juge ni proportionné ni aligné internationalement. La direction soutient qu’un capital plus élevé augmenterait les coûts de financement, limiterait les services et nuirait aux ménages et entreprises suisses. UBS continuera à dialoguer avec les décideurs politiques mais souligne son devoir fiduciaire de protéger les actionnaires.

UBS�� Form 6-K für das zweite Quartal 2025 kombiniert ein solides operatives Momentum mit einer deutlichen Warnung vor den Schweizer Kapitalreformen. Das Management berichtet, dass die extreme Marktvolatilität im April die Performance nicht beeinträchtigte: Die zugrundeliegende Rendite auf das CET1-Kapital erreichte 13,3 % für das erste Halbjahr 2025, die vom Konzern verwalteten Vermögenswerte erreichten mit 6,6 Billionen US-Dollar einen Rekord, und die Aktivitäten der Privat- und institutionellen Kunden waren in allen Regionen stark. UBS gewährte oder verlängerte Kredite in Höhe von 40 Milliarden Schweizer Franken und unterstreicht damit seine Rolle in der Schweizer Wirtschaft. Das Risiko bei der Integration von Credit Suisse sinkt weiter: Alle außerhalb der Schweiz gebuchten Kunden wurden migriert, und die erste Schweizer Welle ist abgeschlossen.

CEO Sergio Ermotti widmet einen Großteil seiner Ausführungen den Bankenreformvorschlägen des Schweizer Bundesrates vom 6. Juni 2025. UBS unterstützt die meisten Maßnahmen, ist jedoch mit dem Kapitalpaket stark nicht einverstanden. Der Wegfall der Konzessionen von Credit Suisse sowie größenabhängige Zuschläge zwingen UBS bereits, etwa 18 Milliarden US-Dollar zusätzliches Kapital aufzubringen; die neuen Regeln würden weitere 24 Milliarden US-Dollar erfordern, womit die insgesamt geforderte Erhöhung 42 Milliarden US-Dollar beträgt. Die daraus resultierende de-facto Mindest-CET1-Quote läge mindestens 50 % über dem Durchschnitt der G-SIBs, was UBS weder für verhältnismäßig noch international abgestimmt hält. Das Management argumentiert, dass höheres Kapital die Finanzierungskosten erhöhen, Dienstleistungen einschränken und Schweizer Haushalte sowie Unternehmen schädigen würde. UBS wird weiterhin mit den politischen Entscheidungsträgern im Gespräch bleiben, betont jedoch seine treuhänderische Pflicht zum Schutz der Aktionäre.

Source: